Article

What's a payment processor? Payments process explained

What is a payment processor, and how is it different from a payment gateway?

The card payments world is full of specific terms that overlap and can be difficult to understand.

‘Payment processor’ and ‘payment gateway’ are two examples that often get confused with each other. They fall into the black box of payments, somewhere between a customer making a payment and the money landing in the business’s bank account.

In this article you will learn about:

What is a payment processor?

What’s the difference between a payment gateway and a payment processor?

How payment processing works as a whole.

Where does Adyen fit in?

What is a payment processor?

A payment processor is a company that processes payments on behalf of a business’s bank. It usually provides the system that enables financial transactions and operates it in the background, making sure processed payments comply with rules and standards in the country that the business operates in. Typically in the payments process, after receiving payment information from a payment gateway, the payment processor communicates it directly to the payment network and authorizes and clears/captures the transaction.

A payment processor plays a critical role in the payments process, ensuring secure payment processing so transactions are handled safely and efficiently.

What is a payment processor example?

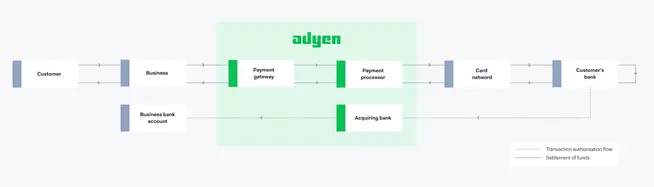

Adyen’s platform is an example of a payment processor, acting as the link between merchants and financial institutions to ensure secure and seamless transactions. Our unified commerce solution simplifies merchant payment processing by connecting all sales channels on one platform. With support for global payments, including credit cards, digital wallets, and local options, Adyen provides a transparent and efficient payment settlement and processing solution for businesses worldwide.

What is a payment gateway and how does it work?

How does payment processing work?

Whether you’re working with an ecommerce payment processor or providing terminals to customers in-store, payment processing only takes a few seconds.

The speed is quite impressive, especially considering the number of steps each transaction goes through:

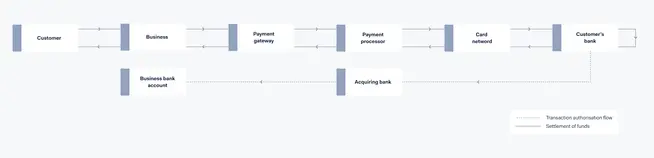

A customer initiates a payment: When a customer is ready to buy, they initiate a payment at the payment gateway. Once initiated, the business sends the customer’s payment information to the payment gateway.

The data gets transformed: The payment gateway transforms the information in adherence to proprietary standards and shares it with the local payment processor.

The data gets shared and checked: The payment processor shares the payment information with the card payment network, which shares it with the customer's bank. The customer’s bank will perform several checks — to see if there are enough funds in the account, for example — to verify the payment.

The transaction gets approved or declined: The customer’s bank will approve or decline the transaction based on the outcome of the checks. The bank will then give that decision back to the card network.

The decision gets routed: The card network will pass the approval or denial to the payment processor. The payment processor will then communicate that decision to the payment gateway, which then displays a message for the business and the customer.

Funds get transferred: Funds from the customer’s bank account will get sent to the acquiring bank, which then sends those funds to the business’s bank account. The transfer typically gets initiated before the end of the day, but the whole process might take 24-48 hours to clear.

How to choose a payment processor

Although payment processing is over in a matter of seconds, quite a few steps happen during this part of the payments process.

Let’s start from the beginning:

After a payment is initiated, the business sends the customers payment information (e.g. cardholder details) to the payment gateway.

The payment gateway transforms the information in adherence to proprietary standards and shares it with the local payment processor.

The payment processor shares the information with the card payment network, which shares it with the customer's bank, which performs several checks, e.g. if there are enough funds in the account. This step is part of payment verification to ensure accuracy and trust.

Based on the outcome of the checks, the customer’s bank tells the card network whether the transaction is approved or declined.

The card network passes the message to the payment processor, which passes it to the payment gateway, which communicates it back to the business and customer to complete the purchase.

The transfer of funds goes from the customer’s bank account to the acquiring bank and then to the business’s bank account and is typically initiated before the end of the day.

Choose your payment processing partner wisely

At Adyen, we simplify and improve online payments and in-person payments for businesses and their customers. We consolidate a payment gateway, payment processor, and an acquiring bank in one platform for both online and in-person payments. Managing payments is easy when you only have one contract and one party to interact with to optimize your business performance.

Our direct connection to global and local card networks will allow you to benefit from local market conditions, improving authorization rates, lowering transaction fees, and strengthening fraud detection in payment processing.

Explore Adyen’s payment-related services and features, such as:

Access to all relevant payment methods globally

Adyen Uplift for revenue boost

Want to learn more? Get in touch here.

Frequently asked questions - Payment Processing

A payment processor is a company that processes payments on behalf of a business’s bank. It usually operates in the background, making sure processed payments comply with rules and standards in the country that the business operates in.

Payment processor companies act as the critical bridge between the merchant’s point of interaction and the complex global financial networks. The processor executes several high-stakes activities in a matter of seconds:

Data orchestration: Receiving encrypted transaction data from gateways and translating it into network-compatible formats.

Network communication: Directly interacting with card networks (Visa, Mastercard) and local payment schemes to facilitate money movement.

Authorization: Managing the real-time logic flow that determines if a transaction is approved or declined by the customer’s bank.

Clearing and settlement: Ensuring transactions are recorded and funds are prepared for transfer into the merchant’s account.