Reports

Marginal Gains #1: Accepting payments

Increasing your authorization rates = more happy customers. In the first of our series on marginal gains we explore some actionable ways to optimize your payments setup and increase authorization rates.

Whether it’sattempting to win the world hotdog eating competitionor Olympic gold in cycling, achieving greater productivity or even overall health: small, incremental, continuous improvements can add up to make big changes.

Dave Brailsford, former performance director for British Cycling, is perhaps the greatest modern proponent of marginal gains.He believed that by making 1% improvement in a whole host of areas, the cumulative gains would end up being hugely significant. This is also the case for improving your payments.

Over the next couple of months, we’ll look at ways you can squeeze the last few drops of goodness from your payments setup and boost your authorization rates. For those of you new to payments, when we talk about authorization rates, we’re referring to the percentage of successful transactions made.

In this first blog of the Marginal Gains series, we’ll explore what you can do to keep authorization rates high, and accept the highest possible percentage of payments.

Making gains by optimizing payments

We know it’s a buzzword, and you probably found this article because Adyen was the first search result for ‘optimizing payments’. We also know that saying optimize starts to lose meaning when you say it more than 7 times. Nevertheless, optimizing payments can mean a variety of things. It could mean offering the right payment methods in relevant markets, intelligently authenticating customers, all the way through to implementing regulatory requirements. Expertise and technology are equally important.

Optimize with payment methods

Geography, demographic, context. These are three of the most important things to be aware of when deciding on the best mix of payment methods to offer your customers. Here’s why:

Geographically

Accepted everywhere doesn’t always mean beloved everywhere. On our platform it’s often the case that the most popular payment method is the one that best suits the locals.

Take M-Pesa’s popularity in East Africa. In a region where 91 million (or 17%) people don’t have a bank account but 75% have mobile phones, M-Pesa succeeds in that it is a mobile network operator that allows users to make payments, transfer money and microfinance purchases. It's so popular that Sub-Saharan Africa accounts for 49% of all mobile money accounts globally.

In Adyen's home country of the Netherlands, iDeal is the local payment method that rules the roost when it comes to ecommerce. The responsibly-minded Dutch are renowned for avoiding credit where possible, so it comes as no surprise that using a secure form of bank transfer is preferred. In this highly lucrative ecommerce market worth €26bn; 60% use this method.

As the diagram above shows, payment method usage varies from country to continent and their popularity can be dependent on many factors. In Kenya, it could be a lack of access to banking facilities, while in the Netherlands it could be due to an aversion to credit cards. In other regions, accessibility to the internet, and even the age of a given population are factors in the payment mix.

Demographically

In her 2019 article for Adyen, Sheryl Kingstone, Vice President of 451 Research touched on the need for fashion brands targeting millennials to capitalize on social media reach. She argued that if the first impression millenial shoppers make is via a social media platform, then fashion brands should utilize "shoppable" advertisements. This allows the brands to instantaneously accept payment and convert a browser into a buyer.

One way to cater to the younger demographic is through enabling ewallet payments. It’s obvious, but the 16-34 demographic is mobile obsessed. So, allow these shoppers to pay with tokenized card details saved conveniently to their mobile wallet. specific examples include Google Pay ™ , Apple Pay, and Amazon Pay. Their connection to the relevant app store, browser, or ecommerce account means shoppers can pay via ecommerce, social media, as well as in-store.

To put this into perspective, research suggeststhat by 2023, there will be 1.31 billion people using mobile payments.

Contextually

Assess how your product or service might impact the payment method your customers choose. Take buying a car as an example; the product is of high value, so the customer is more likely to use a method with flexible payment options e.g. installments. They’re much less likely to pay, in-app, or via debit card. Subscriptions are different, with a low average transaction value (ATV), so we advocate for set and forget options (direct debits or stored credit cards) while optimizing with tokens.

Adyen tip: Our unified platform makes it easy to try new payment methods (often without additional contracts) and through our merchant network we have a range of performance insights for all industries, business types, and countries to help you get an optimal mix. Our philosophy is based on quality and performance over quantity, but we encourage merchants to experiment with payment methods based on their needs.

Optimizing the authentication experience in times of PSD2

Once the shopper has hit “pay”, authentication may come into play. Conversion is now your number one concern, followed by meeting regulatory requirements like The Revised Payment Services Directive (PSD2). PSD2 is a European regulation, introduced to make payments more secure.

We developed our 3D Secure 2(3DS2) solution to improve authentication flows and save businesses time figuring out the different regulatory landscapes in each region. It also makes the authentication process less tedious for customers.

In the bygone times of 3DS1, shoppers would be redirected by their bank to a page where they’d be asked something banal like a memorable name, their mother’s birth-name. Basically something easily forgettable. This led to the less-than-ideal scenario of many customers abandoning their shopping carts.

3DS2 makes it easier to accept payments. The combination of certified SDKs in the checkout flow, paired with data sharing APIs means that merchants and banks can share data in the background with limited interruption to the customer’s checkout experience. The option to build a native 3DS2 experience limits the need for shoppers to be redirected to a non-native authentication page.

In short, it optimizes the checkout and often increases authorization rates.

For payments involving European shoppers, PSD2’s Strong Customer Authentication(SCA) requirements will come into effect soon. These are: something you know, something you own, something you are. This combination makes authorization easier because, well, you can’t forget your thumbprint can you?

There are also a couple of exemptions that can make things even more straightforward.

- Low risk, low value, and subscription-based payments are exempt from SCA

- Shoppers also now have the option to select a list of ‘trusted beneficiaries’ that can be saved by their bank, so that they forgo 3D Secure. E.g. you’re buying 20 bars a week from Tony’s Chocolonely’s webstore - of course you trust them.

Keep customers happy and secure

The gains that come from keeping customers happy and secure are more than marginal. By combating fraud at the authentication stage you can reduce the loss of trust, the effort that comes with actioning chargeback disputes, and you can keep authorization rates high for genuine authenticated customers.

Adyen tip: RevenueProtect allows you to add an Authentication risk rule. You can customize a warning for transactions in high-risk locations, industries, or even on individual types of transactions you see as potential fraud for your business.

Optimizing the application of authentication

Authentication can be a complex business. Working with different issuing banks and regions requires different approaches. And you don’t always have the time or resources to keep track of all these real-time changes. We built Authentication Engineto offer a unique approach in unraveling all the complexity from different issuing banks into accurate routes to authentication that leads to higher authorization rates.

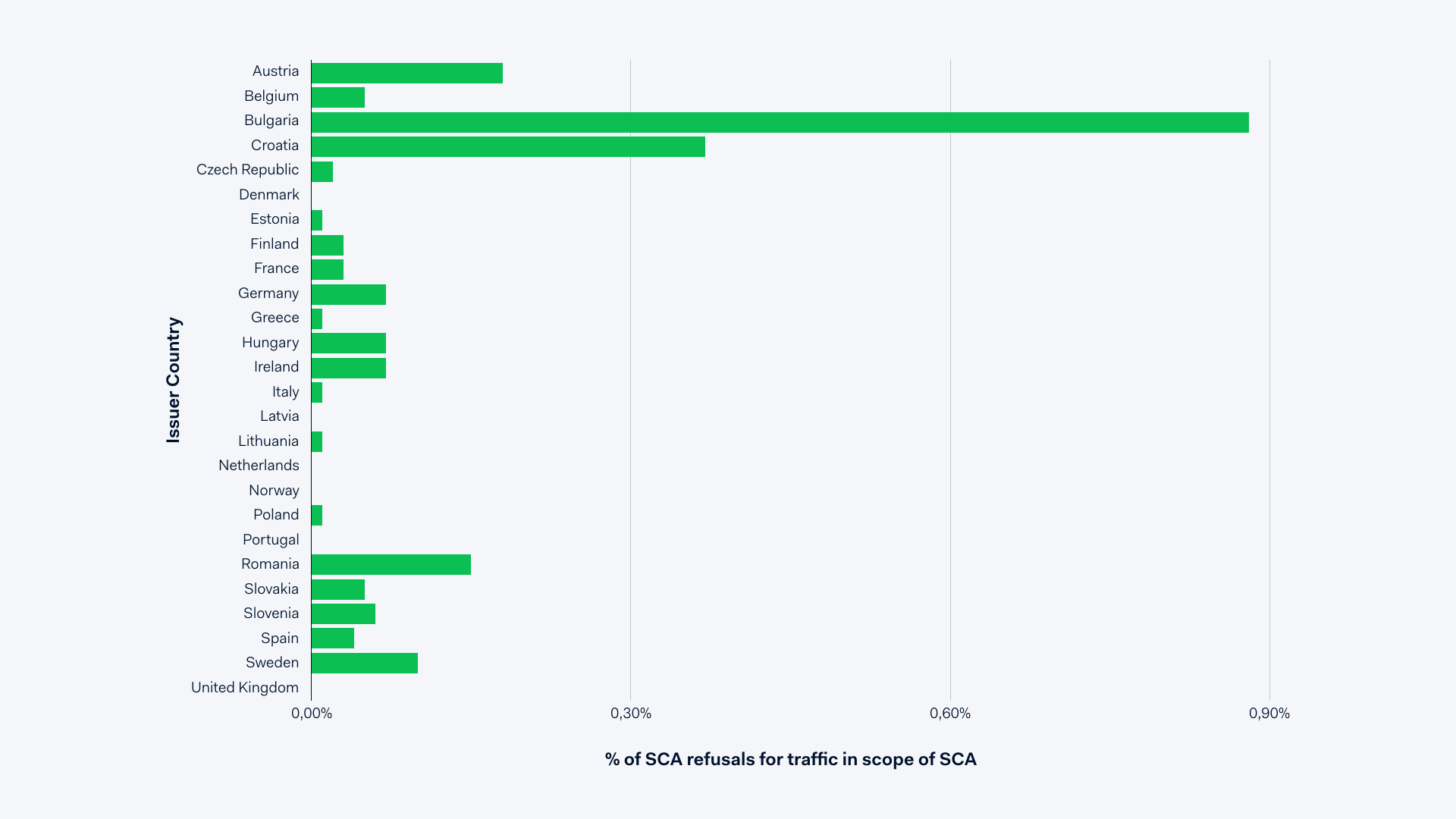

The chart below illustrates the percentage of declined payments due to SCA requirements ahead of PSD2 enforcement deadlines. Using our Authentication Engine, these payments will be automatically retried with SCA so that the shopper can complete their purchase.

There are key aspects to look for when understanding how authentication application can be optimized:

Funneling the authentication flow

There are two checkpoints to a payment: authentication and authorization. It’s at the cross section of these two checkpoints that 3DS comes into play.

Checkpoint 1: Authentication and the merchant.The provider of your 3DS2 solution knows what works best for your business and customers. This can be based on locale, payment method, device, and more.

Checkpoint 2: Authorization and the acquirer.When it comes to card issuers, the acquirer knows what version of 3DS works best for the highest authorization rates. The merchant and acquirer are often separate entities, which can cause a disconnect and a higher likelihood of declined payments.

Every payment is unique, so a full view of the transaction can be really important when striving for the highest authorization rates. This is the basis of our end-to-end solution.

Adyen tips:

Apply exemptions within the payment process.These reduce the risk of payments being declined by an issuer and the merchant having to process the payment twice. Processing a payment twice can be costly; it means two transactions, twice the costs, and the potential to inconvenience your customer.

Make sure you’re up to date from a regulatory standpoint.Look for options that use machine learning to assess large datasets and optimize in real-time. This means you don't lose out just because an issuer has made a change at their end or if a new exemption comes into play.

Accept, protect, process, and recover

We’ve now covered some of the ways to boost your rate of accepted payments. Keep your eyes peeled to our blog over the next couple of months. We'll be covering ways to protect shoppers, processing payments, and recovering declined payments.