Article

Insurance payment processing: Uncover a new competitive edge

How insurance payment processing can be optimised to improve customer acquisition, ensure retention, streamline operations, and drive growth.

A recent article by Raconteur tells us that, as of 2024, digital transformation has been on the business agenda for over a decade. But, while some industries are steaming ahead, InsurTech points out that “when it comes to digital transformation, the global insurance industry is a touch late to the party.” That may be so, but in the UK, against the backdrop of Lloyd’s Blueprint 2, the industry is stirring into action.

But for many, digital transformation remains an item on an already crowded to-do list, as Chris Payne, EMEIA Insurance Technology Leader at EY explained:

“There are a range of dynamics at play across the insurance sector. Digital transformation is a critical focus for firms, although the costs and complexity involved, alongside the current challenging economic environment, mean the speed of progress is mixed. Insurers also remain focused on creating and sustaining customer loyalty. Key to this is unlocking actionable, data-driven insights to offer customers relevant solutions and improved experiences. The industry also remains focused on the sustainability agenda and keeping pace with regulatory change.”

So, how can insurers remain competitive in a market where consumers are more technical, more impatient, and more focused on sustainability?

Often overlooked is insurance payment processing. Whether you’re collecting premiums or paying out claims it is a critical customer interaction. In a world of price comparison sites, it’s common that the only touchpoint with your customer is when they pay for their policy. This makes it a vital moment in which to demonstrate your value and establish trust.

But too often insurance payment processing falls short. Fragmented systems and siloed payment methods make the process slow and clunky. Recurring payments fail causing customer churn that you only find out about when payment is late.

In this article, we’ll explore what digital transformation looks like in the context of insurance payment processing. And we’ll uncover how a modern payments infrastructure can protect your revenue and drive growth by:

Supporting customer acquisition

Improving customer retention

Streamlining business operations

Unlocking new growth opportunities

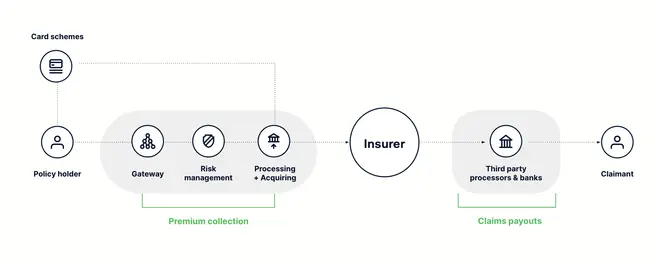

Payment processing for insurance companies

When it comes to insurance payment processing, there are two main touch-points: Collecting premiums and paying out claims.

Collecting insurance premiums

The act of taking your customer’s money for that initial premium payment might be the only interaction you have with them. No matter how they land on your checkout page, it’s important you close the sale. At the very least, you’ll want to recoup the investment you made to bring them there in the first place.

However, a recent study found that finance companies (which included insurance) have the highest cart abandonment rate (84% compared to a general average of 70%). And, according to our own research, “up to 55% of consumers abandon purchases if they can’t pay using their preferred methods”. So, it’s important to get the payment experience right.

To understand the state of insurance payment processing today, we collaborated with EY to gather a focus group of leading UK insurers. Based on the insights from that discussion, below is a summary of the current state of the insurance payment experience:

Direct debit: Very common form of collecting policy payments

Pros

Well-known and trusted method amongst customers

Cons

Set-up is cumbersome

Payment is not instant

Call centres: Still used by most insurers

Pros

Popular amongst older demographics

Cons

Vulnerable to fraud and often not PCI-compliant unless payment links are used

Cards

Pros

Widely used payment method

Cons

Can have a high failure rate, especially if not processed correctly

Open banking: Emerging method gaining in popularity

Pros

Low failure rate and instant settlement

Cons

A relative newcomer; might alienate older demographics

Pros

Secure payment method with high authorization rates

Cons

Potential compatibility or integration issues if not supported properly

Paying out insurance claims

In the UK, one of the few places you’ll still see cheques being used as means of paying out insurance claims. Another popular method is Bacs transfer. However, a report by the Association of Financial Professionals, sponsored by JP Morgan, found that “cheques and wire (Bacs) transfers continue to be the payment methods most impacted by fraud activity (66% and 39%, respectively).”

Slow and high-risk payouts have no place in a modern insurer/customer relationship, especially during a time of economic fragility. An open letter to UK insurers from the Financial Conduct Authority (FCA) further underlines this point. Customers expect (and deserve) speed, efficiency, and transparency in their interactions with businesses. Sluggish, outdated payouts won’t just harm the customer, they will eat away at your competitive edge.

The industry is ready for something new and financial technology is here to help take insurance payment processing to the next level.

Payments to protect revenue and drive growth

Payments can be a powerful competitive advantage for insurers. The right setup will help with onboarding new customers, reducing customer churn, keeping costs down, and even generating new revenue streams. Here’s how:

Customer acquisition

Today, customers can order a taxi, book a holiday, or send out for a pizza with a few taps of their finger. One-click or even zero-click payments are now standard in most interactions. Delivering such experiences demonstrates an organisation’s willingness to meet customer expectations. It’s also critical to securing high conversion rates. Here are a few ways payments will help boost your customer acquisition:

Optimised checkouts

Encrypted payment fields embedded into your checkout pages allow you to handle the whole payment from your site (avoiding the dreaded redirect). These fields can dynamically offer a range of relevant payment methods based on your customer’s location, device type, and even their installed apps.

Payment links for call centres

Whether you’re serving a customer who prefers to pay over the phone, or you’re following up on a failed online payment, your call centres need a secure way to take payments. With a payment link, your customer no longer needs to read their card details out over the phone. Instead, you issue them a bespoke payment link via text or email that takes them to a secure online environment where they can complete the payment. Learn more about payment links >

End-to-end processing

Do you know why your card payments fail? And, if you did, would you be able to do anything about it? If your gateway and acquiring are handled by the same provider, you’ll get information directly from the issuer about the reason behind a decline. If it was due to a formatting issue or a temporary failure in the bank’s system, the payment can be saved by retrying it again immediately.

Related: https://www.adyen.com/en_GB/knowledge-hub/acquiring-bank

Smart authentication

Successful risk management is all about finding the sweet spot between security and conversion. You want to block fraud but you don’t want to create unnecessary barriers for your genuine customers. Strong customer authentication, such as 3D Secure, used to be known as the ‘conversion killer’. But thankfully today, machine learning ensures only ‘in scope’ transactions get passed through the additional security layer. And, when authentication is necessary, biometrics keep the process quick and easy.

Note: Digital wallets such as Apple Pay, come with authentication built-in as standard, making them very secure payment methods with high authorisation rates.

Related: https://www.adyen.com/en_GB/knowledge-hub/psd2-understanding-strong-customer-authentication

Our solution: Our online checkout is designed to boost conversion at every step with all key payment methods available via a single integration. We have local acquiring licenses in all major markets. And our suite of optimisation tools ensures you squeeze more revenue out of every transaction.

Customer retention

The biggest concern with recurring payments is that they get dropped and no one notices until it’s too late. This can be a serious issue if someone believes themselves to be insured when in fact they’re not. It can also be a drain on resources spent chasing on failed customer payments. Fortunately, the following payment technology can be used to minimise the damage:

Account Updater

A key cause of failed recurring payments is lost, stolen, or expired cards. To solve this, the card schemes developed Account Updater services that let businesses and acquirers replace invalid card numbers with new ones. The first iteration of this solution, which is still used widely by many insurers today, updates card details in batches. This is fine, as far as it goes. But the technology has moved on. Real Time Account Updater services instantly check with Visa and Mastercard for updated card details and, if there's an update, will immediately retry the payment with the correct details.

Network tokens

Technology has come a long way since a Primary Account Number (PAN) was first embossed onto a credit card in 1959. Now, known to fuel a rampant trade of stolen credit card information and fraud, the PAN is being retired and a new technology taking its place: network tokenization.

Network tokenization replaces the PAN with a network token that can be used to authorise online and recurring payments. If your customer chooses to save their card details, you can request a network token for that card to use for future payments. And, since network tokens don’t expire, the token will remain valid even if the issuer replaces the card. These tokens can only be used by the party that requested it which means they’re useless if stolen.

Given their heightened security and immunity to lost/stolen card issues, tokens are increasingly popular with issuers, leading to higher authorisation rates. Plus, while the card schemes might charge a fee for the management of issued tokens it will be lower than the fee for processing PANs - so you’ll be saving money too.

Optimized billing

If a payment is declined due to ‘insufficient funds’, it’s tempting to assume game-over. However, a high rate of these declines could suggest your billing strategy needs tweaking. It’s common for recurring billing to be tied to the date the customer signed up. But, if this falls just before payday, you’re requesting funds when they are least likely to be available. Adjusting your billing to fall just after payday, will likely lower your ‘insufficient funds’ decline rates. Alternatively, you can give customers the option to choose when they are billed each month.

Our solution: With years of experience working with the likes of Uber and Spotify, we have a deep understanding of recurring payments. We were the first to launch Real Time Account Updater with Visa in Europe. And, with two billion active network tokens on our platform to date, we’re helping our customers move to network tokenization seamlessly.

Streamline operations

The traditional payment value chain combines a patchwork of different systems, each with their own integrations, their own fees, and their own points of failure.

A modern payments infrastructure removes the need for these legacy siloed systems. If you have a single provider handling your gateway, your acquiring, and your risk, you’ll have just one integration, one set of fees, and one support number to call. Reconciliation becomes much easier since you have a single view of your payments. Plus, if your provider supports online and in-person payments and has global acquiring capabilities, all your payments across all channels and regions will feed into a single back-office system.

Connected systems also pave the way for connected data. Payments data has huge potential to unlock important insights such as monitoring authorisation rates. And, of course, consolidation also leads to agility. With a single payments provider, you’ll have a more streamlined tech stack, which allows you to scale fast and respond to consumer trends quickly.

Our solution: Since its inception, Adyen has set out to dismantle the traditional payments value chain and replace it with a single solution designed to support business growth. By consolidating your payments with Adyen, you’ll streamline your operations, removing integration and reconciliation burdens from your tech and finance teams.

Unlock new growth opportunities

With payments set up right in the backend, you’ll be free to explore new growth opportunities such as faster expansion into new channels and markets. The right partner will also ensure you stay on top of ever-changing regulations across different regions. PCI will be kept to a minimum and you should be kept on top of the latest updates from the EU Payments Services Directive (PSD3). Plus, you’ll have powerful data insights to drive growth decisions.

But it doesn’t stop there.

Improving payouts for the insurance industry with embedded finance

In recent years, embedded finance has become a powerful way for businesses to solve age-old problems, while introducing new revenue streams. A perfect example improving the handling of payout claims through issued cards.

Physical or virtual cards could be issued to customers, pre-loaded with the approved amount, and restricted to a list of approved suppliers. Customers can use the card to pay the relevant service provider. And, if there is any money left over, it can’t be used for anything else, reducing claims leakage. This added control not only helps to reduce insurance fraud, but you’ll also benefit from the split of interchange fees (upwards of 1.5%), helping you offset the cost of processing payments.

Our solution: Adyen is a fully licensed financial institution in the UK, US, and EU, which means we can offer embedded financial products, such as card issuing, to our customers. This includes expense management (with a revenue split in favour of our customers). We are also leading experts in regulation and compliance across all key global markets. We keep tabs on changes to mandates so our customers don’t have to and we do the legwork to ensure you’re always up-to-date and compliant.

How can Adyen help with insurance payment processing

One of the main reasons our customers, such as Uber, Spotify, Ebay, Body Shop, and Epos Now, value us is that we offer them a ‘subscription to innovation.’ Signing with us provides much more than a payments integration; it secures a promise that our customers will always be at the forefront of financial technology innovation. That’s why we’re trusted by the world’s leading companies to help them achieve their ambitions faster. These include insurers such as Cover Genius, Allianz, Liberty Mutual, and Clear Cover.

Our global regulatory framework, including acquiring licenses and banking infrastructure, coupled with our proprietary technology, allows us to provide the best possible financial solutions to customers across multiple regions and industries.

And finally, by partnering with Adyen, you’ll have access to a team of experienced account managers, backed by industry-leading experts in conversion, data science, risk management, and acquiring. Together, we’ll ensure you offer the best experiences to your customers and your business is optimised for growth.