The OTA Playbook

Reinventing money movement in travel

The changing landscape of travel commerce

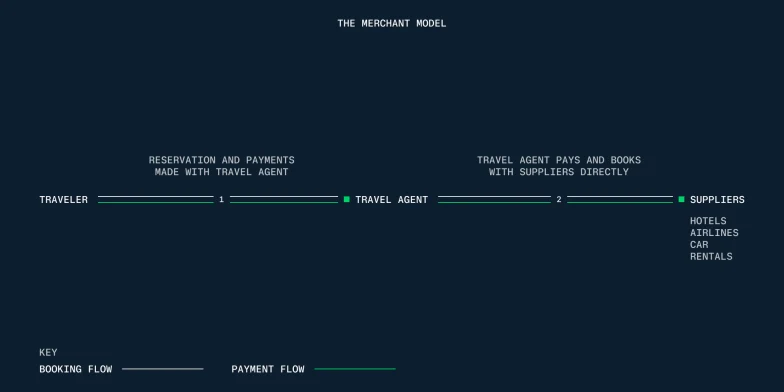

The agency model

Global travel is entering a new phase of expansion. Digital distribution continues to reshape how bookings are made, and online travel agencies (OTAs) have strengthened their position at the center of this ecosystem.

But the most important change is not just how travel is booked – it’s how money flows across these platforms. OTAs have historically operated under the agency model. This is where the supplier remains the merchant of record and is paid directly by travelers. The OTA earns commission after the booking, limiting access to upfront cash and increasing pressure on working capital as volumes grow. A report by Onyx CenterSource, a global leader in commission payments for hotels, highlighted that on average, it takes 42 days for OTAs to be paid commission. [1]

The rise of the merchant-of-record model changed that dynamic entirely. Under this model, OTAs collect funds at the point of booking and settle with suppliers at varied timelines – sometimes almost immediately, in other cases at check-in or even after the stay.

During periods of growth, this creates a clear liquidity advantage. But that same flexibility can quickly become a constraint, depending on the supplier being paid and the settlement terms in place.

The merchant model

While many large platforms operate on hybrid structures depending on corridor, supplier type or product category, the merchant-of-record model is the most common and has redefined the role of OTAs. They now sit between traveler demand and supplier fulfillment, managing the full lifecycle of the transaction.

Money movement now underpins the industry’s primary business model.

However, travel demand is inherently volatile. This is particularly relevant for platforms designed for easy comparison and flexible booking, as customers can reserve multiple options and cancel later with minimal friction. As a result, OTA cancellation rates for hotel bookings reached 21.8% in 2025, more than double the 10.6% rate for direct bookings. [3] This creates significant risk, as liquidity can quickly shift to refund exposure.

This volatility also affects OTA’s access to short-term credit and impacts traditional lenders’ perception of the industry. Not only are market conditions and demand in constant flux, but global travel shutdowns in recent years have heightened caution.

As OTAs expand internationally, complexity compounds. Payments move across currencies, jurisdictions and regulatory environments, with transactions between countries significantly outpacing domestic volumes.

Handling complexity on both sides of the flow

Evolving customer behaviors

As OTAs expand across markets, travelers expect localization in payment methods, experiences and offers. Cards, digital wallets, and alternative payment methods now coexist within a single booking journey. When OTAs act as the merchant of record, this diversity falls directly within their remit. They must optimize consumer pay-ins across currencies, schemes, and methods, all while controlling acceptance costs to protect already thin margins. Generative AI and Agentic Commerce are also beginning to reshape how travelers discover, book, and pay for travel. Instead of navigating OTA platforms directly, users can increasingly search, compare and complete bookings through conversational interfaces. [7] This introduces a structural risk. As AI agents take a more active role in the journey and ownership of customer relationships fluctuates, OTAs risk losing visibility, and ultimately influence, over the booking experience, becoming embedded within third-party ecosystems. [8] In this environment, the room for error narrows. OTAs must deliver seamless, localized payment experiences to retain customer attention and trust.

The challenge of paying suppliers

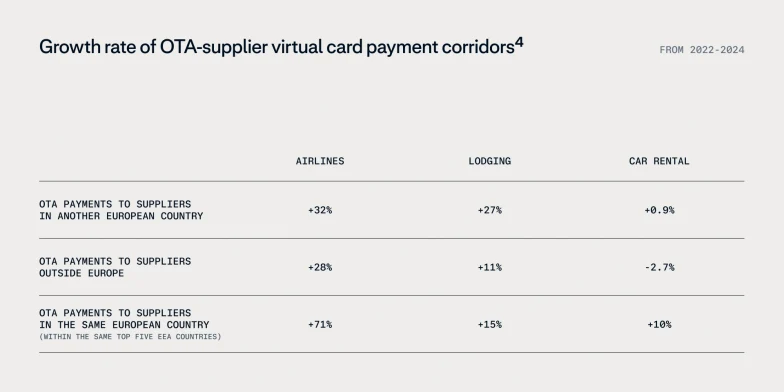

Supplier payments are far from standardized. Airlines, lodging providers and car rental companies all operate on different settlement models. Airlines typically require near-immediate payment, while accommodation providers are often paid at check-in or even after the stay. The way suppliers manage payments also varies by supplier type. In the airline ecosystem, payments are often routed through Global Distribution Systems (GDS), which act as the core booking infrastructure for intermediaries. In lodging, Property Management Systems (PMS) play a similar role, delivering virtual card details and booking data in a format suppliers can process and reconcile. Together, these systems add another layer to how funds and data move between parties. On top of this, as OTAs scale globally, they must manage payments across a diverse supplier base spanning multiple geographies, currencies, and time zones. This introduces additional friction, particularly as pay-in and payout flows become increasingly disconnected. In this environment, supplier payouts are no longer just an operational necessity – they are a revenue driver. Optimizing how and when suppliers are paid has a direct impact on cash flow, cost control and supplier relationships, especially as traditional methods struggle to support cross-border scale and speed. As a result, many OTAs have integrated single-use virtual cards to manage this complexity. These are issued for a specific supplier, amount and booking. One regional OTA reports that more than 60% of its payouts to vendors, suppliers and partners are executed via virtual cards. [9] This method allows for precise control over each transaction, simplifies reconciliation and supports automated, one-to-one settlement between booking and payout. Alongside paying a fragmented supplier base, OTAs must now account for different supplier types growing across different payment corridors.

Airlines are driving strong domestic acceleration, lodging is expanding intra-Europe, while car rental shows mixed growth.

As these dynamics converge, OTAs are no longer managing isolated payment flows, but an interconnected system spanning both pay-ins and payouts. This creates a dual challenge: delivering seamless, localized experiences at the front end while maintaining tight control over costs, liquidity and settlement behind the scenes. When these flows are managed separately, the result is a disconnect that impacts cash flow and constrains working capital.

The impact of fragmented systems

The cost of disconnected payments

The complexity of OTA payment flows is hard to manage in practice. Many still operate across multiple systems, with acquiring, issuing and reconciliation handled separately.

As volumes grow, disconnected systems move from an operational inconvenience to a financial strain, creating margin pressure, cash flow constraints and reconciliation and operational drag.

Margin pressure

OTA margins are shaped by both sides of the transaction: the cost of accepting payments and the cost of paying suppliers. To offer competitive pricing to travelers, OTAs must be able to pay suppliers efficiently, even as cross-border transactions and FX spreads add significant pressure. Local optimization plays a critical role, as OTAs need to be able to accept payments from local acquirers and settle funds in local currencies. 71% of airline and online travel businesses are losing out on major savings by not working with local acquirers to process payments. [10] However, local payment methods can offer an average cost saving of 49% compared to credit and debit cards, which would help OTAs balance customer preference with commercial efficiency. [11]

Cash flow constraints

The merchant-of-record model introduces a structural timing gap between when customer funds are received and when suppliers must be paid.

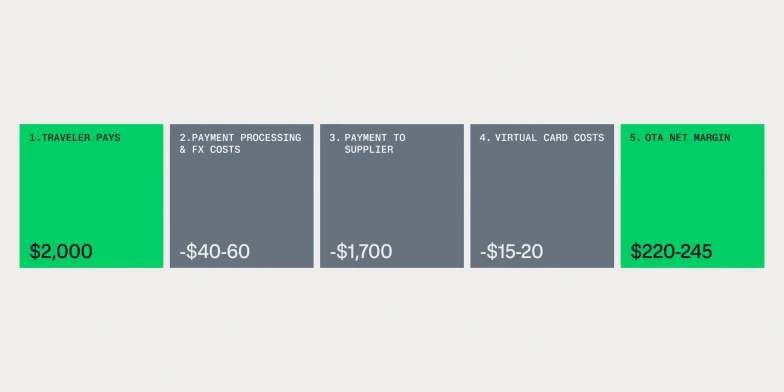

In practice, this gap can be substantial. As one OTA described: a customer books on day 0, but the OTA may wait up to three days for funds to settle, while the ticket must be secured instantly. [12]

When pay-ins and payouts are managed separately, it becomes harder to see and use available cash in real time. This reduces financial flexibility and means OTAs often need to rely on credit lines or pre-funding to bridge the gap between receiving customer funds and paying suppliers.

A single booking is manageable. But as volumes grow, countless payments to different suppliers, often required at the same time, place increasing strain on liquidity.

Reconciliation and operational drag

Reconciliation remains resource-intensive for many OTAs.

36% of global enterprises lose at least one full day of work on global payment operations.

Interviews with OTAs consistently describe the same pattern: multiple CSV exports at day-end, manual consolidation into ERP systems, and transaction-level investigations to understand fees, exceptions, and settlement differences. [12]

Working with multiple PSPs and third-party banks across acquiring and issuing, alongside separate systems for cards, bank transfers, and local payment methods, make it harder to consolidate data and resolve discrepancies efficiently.

The result is inconsistent reporting, a higher volume of refunds and disputes requiring manual intervention, and significant time spent resolving issues rather than improving performance. This has a cumulative effect of increasing pressure on treasury management.

A connected future

The complete money lifecycle

Leading OTAs are thinking beyond payments and considering the complete money lifecycle. This means bringing pay-ins, cash management and payouts onto a single platform, allowing them to accept payments from various channels and connect this directly to supplier payouts.

The ideal state goes beyond adding more tools, and is achieved by reducing fragmentation and unifying acquiring, accounts and liquidity management, as well as issuing and treasury.

Key benefits

Visibility Treasury teams gain real-time visibility into cash positions across regions and currencies. A unified view of inflows, outflows and balances enables more accurate liquidity forecasting as settlement timelines are reduced or standardized. This strengthens control over working capital, improves financial planning and allows teams to make faster, more informed decisions.

Speed Time is reduced between receiving funds and being able to use them. Optimized payment routing, local processing and accelerated settlement (either same-day settlement or on the next business day) to fund payout and virtual card flows directly improve cash flow, financial flexibility and manual processing costs. Working capital is no longer tied up, and reliance on credit or pre-funding is reduced.

Efficiency Operational complexity decreases, with fewer PSP integrations, centralized fraud and dispute workflows, and automated reconciliation reducing manual effort and stabilizing costs. A connected acceptance strategy also enables smarter payment method orchestration by allowing OTAs to route transactions dynamically across methods, markets and providers.

Historically, achieving this level of unification has been difficult due to legacy systems and organizational silos. Overcoming these barriers depends on partners that can operate across acquiring and issuing with the volume, resilience and control required by global OTAs.

How Adyen and Visa support OTA growth

Connecting demand to payouts

A unified payments strategy requires more than point solutions. It depends on deep connectivity between acquiring and issuing, global expansion and a clear understanding of travel payment flows. Adyen provides a single end-to-end platform that connects acquiring, accounts and liquidity management, as well as issuing and payouts, all purpose-built for complex, high-volume merchant models.

Since 2023, Adyen has held full banking licenses across its core markets, including the EU, UK and US. This enables direct control over liquidity and settlement, eliminating dependency on third-party or sponsor banks. This infrastructure is the foundation for Intelligent Money Movement, Adyen’s enterprise offering that provides faster, more flexible fund flows and real-time capital management tailored to customer needs.

Visa brings global acceptance, insight into travel corridors and established capabilities in B2B travel and virtual card economics. With infrastructure that supports reach across more than 200 countries in approximately 160 currencies, Visa has solutions designed to streamline global logistics, reconciliation and spend visibility for travel intermediaries. [13] [14]

Together, Adyen and Visa help OTAs connect consumer demand to supplier payouts more efficiently, enabling scale while reducing operational drag.

Streamlining lastminute.com's global payouts

Lastminute.com is a pan-European OTA with more than 25 years in the market, offering flights, hotels and holiday packages across multiple markets and currencies. Whilst their customer checkout experience was seamless, supplier payouts behind the scenes were highly complex.

By partnering with Adyen, supported by Visa’s B2B travel solution, global acceptance and expertise, lastminute.com brought pay-ins and payouts into a single platform.

"OTAs operate across fragmented corridors, multiple currencies and complex payout models. We’ve built our platform to unify acquiring, money management and issuing around those realities, helping OTAs simplify operations and scale with greater financial control. Visa’s global network and expertise further strengthen that capability, enhancing performance and scale."

"By working in close collaboration with Adyen, we’re helping them bring OTAs greater consistency and intelligence to their payments infrastructure through thought leadership and industry knowledge. Together, we’re streamlining the flow of funds end-to-end, reducing friction, strengthening security and enabling global scale."

"Adyen’s partnership with Visa has been a key enabler. Visa’s B2B travel solution made everything more efficient and cost effective. Our finance teams spend less time on the reconciliation process, and we’ve increased the income impact of pre-funded cards by 6%."

Conclusion

The next step for OTAs

The merchant-of-record model has reshaped the travel ecosystem. But as they scale, the challenge is financial orchestration.

For OTAs entering the next phase of expansion, reducing fragmentation and improving financial efficiency will be critical to strengthening control, protecting margins, and supporting sustainable growth.

Adyen is trusted by the world’s leading suppliers and Online Travel Agencies. We drive value across traveler and supplier experiences by simplifying global payment operations and cash flow management.

Citations

References

[1] Onyx CenterSource. 2025. “Onyx Quarterly Check-In: Hotel and Travel Agency Commission Trend Report" - Q3 2025.

[2] The agency model: The time of payment required varies by supplier. [3] Cloudbeds. 2026. “Cloudbeds Unveils 2026 State of Independent Hotels Report.” March 25, 2026.

[4] Visa Adyen_Issuing OTA Market Strategy – Final Report (1)

[5] Adyen Index Digital Report 2024

[6] Adyen Index Hospitality Report 2024

[7] Barron’s. 2026. “AI Fears Slam Booking and Expedia Stock. Why They Can Bounce Back.” February 6, 2026.

[8] Adyen. 2026. “Agentic commerce has an infrastructure problem.”

[9] Visa Consulting & Analytics. 2025. Internal research: Series of seven industry interviews with OTA and supplier finance experts (Europe and North America).

[10] Adyen. 2024. “How to reduce your total cost of payments.”

[11] Adyen. 2024. “Adyen Index Survey Data.”

[12] Interviews from VCA.

[13] Automated Reconciliation: Financial reconciliation from days to hours

[14] Visa. 2025. “Annual Report 2025.”

[15] Visa. 2023. “Empower Smarter B2B Payments.” Visa.co.uk. 2023”

Modernize travel payments

Streamline your payments, manage cross-border liquidity, and accelerate supplier payouts.