Article

Optimizing supplier payments: A new way of issuing virtual cards

Discover how to optimize supplier payments through a new way of issuing virtual cards.

If you’re a business making supplier payments, you've likely embraced virtual cards as an automated and reliable solution for delivering funds to your suppliers in real-time. Now is the time to explore how to optimize your setup and pioneer new ways to pay suppliers using virtual card issuing.

We've identified three important elements that are crucial to optimizing your setup. This guide will help you uncover an opportunity to speed up cash flow, increase reliability, save costs, and drive more revenue.

Before we dive into how you can optimize your setup through a new way of supplier payments using virtual cards, let's look at the typical card setups for businesses.

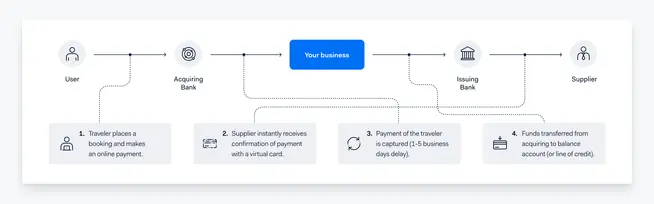

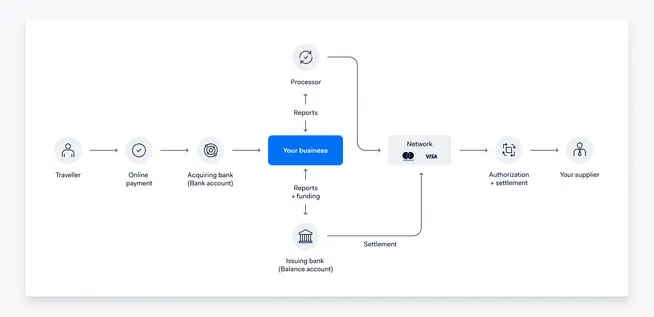

Virtual cards for your business

Whether you’re looking to pay hotels, airlines, or any other business supplier, the goal remains the same: fast and reliable payouts.

A virtual card program for paying suppliers works for a variety of businesses. The setup generally looks the same:

Businesses like online travel agencies and other types of marketplaces often use this setup for supplier payments, and you may have something similar that works for you. However, there are exciting optimization opportunities that can help save time and money.

How to optimize your setup

If you're using virtual cards to pay your suppliers, there are three key areas that are central to continuing to optimize and ensure cash flow efficiency for your business and an enhanced experience for your suppliers.

Automation and reliability

Suppliers expect to get their funds on time, every time. As a business operating globally, a reliable and automated payment setup is essential to your business model and building and retaining your suppliers' trust.

Businesses can decrease the risk of errors by reducing the number of third parties involved in the payout process, improving automation, and increasing reliability.

One way of doing this is by choosing an aggregator provider. Aggregators claim to only have one agreement and one integration, even though multiple third parties are often involved. The advantage of an aggregator is that they manage the relationships with the other parties. However, since multiple parties are involved, there is a higher risk of errors.

At Adyen, we don’t rely on third parties. We create a seamless payout process by combining issuing and acquiring in one platform. We've built our infrastructure and licensing from the ground up with enterprise businesses in mind.

Funding

Virtual cards need funding to pay suppliers. Choosing the wrong type of funding can increase costs and act as a barrier to growth.

There have traditionally been two options to fund your virtual cards. One option is to fund your balance account with working capital. The downside of this approach is that the working capital is inactive on your account instead of using it to invest in your business.

The second option is funding through a line of credit service, a service offered by issuing banks in which they extend the credit when a payment is made. Because credit lines are technically loans, they’re often expensive and unreliable.

There is a new and unique way of funding virtual cards that doesn’t require inactive working capital or line of credit services. By combining acquiring and issuing in one platform, businesses can seamlessly bridge incoming funds with outgoing payments to virtual cards for paying suppliers. This makes incoming funds instantly available for outgoing card payments.

Acceptance rates

When a traveler places a booking, they want it confirmed instantly. To do so, you need to make a successful payment to the supplier so they can reserve the hotel room or flight.

When a payment is declined, another attempt is made to complete the payment so the booking doesn't fail. This causes friction in the process and negatively impacts the user experience.

One way to optimize acceptance rates is by choosing the right card product for your program. A card product is defined by the network it operates on, like Mastercard or VISA, the bank identification number (BIN) range. It can also be identified through other operational variables, like whether it's a commercial or consumer card. Certain card products are often declined in the travel industry. Knowing which ones to choose for your program to increase acceptance rates can be difficult if you don't have the right insights.

Understanding what card products are accepted or declined by certain suppliers can help you choose the best option. At Adyen, we help many businesses in the travel sector with acquiring. This means we understand what type of businesses accept which card products. We can work closely with you on your program and advise which card products work best for your business.

In the majority of European countries, we can issue cards domestically. This increases the acceptance of your suppliers because domestic processing costs are much lower for them.

Finding the right provider for your business

Navigating between banks, issuers, and fintech providers can seem challenging. Choosing a provider that aligns with the key performance drivers above is important to optimize your supplier payments and ensure cash flow efficiency and an enhanced experience.

Let’s look at the pros and cons of the most common setups for supplier payments, including a completely new way of issuing and what benefits it can bring to your business.

Processor only

With this setup, the provider is only responsible for processing card payments. You manage your card program and all the partnerships involved. This means you need to find your own bank partner, manage the approval of the card program with the bank and card networks, and ensure compliance.

Pros:

Good geographical coverage

More flexibility in choosing partners

Cons:

Multiple-party setup, which increases the risk of errors

Added overhead costs for managing third-party agreements

Additional costs due to managing funding

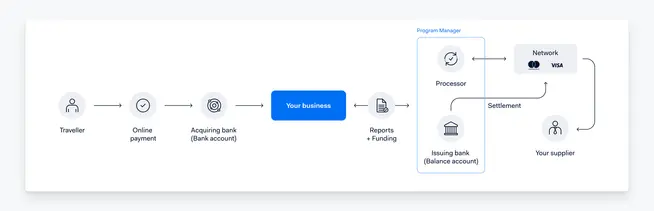

Program managed

With the program managed setup, the provider is responsible for your card program and the partnerships. This setup removes a lot of the complexity of managing a card program.

Pros:

Provider manages licenses and agreements with third parties

Fewer resources are needed for infrastructure set-up and maintenance

Good geographical coverage

Provider takes care of program approval and compliance

Cons:

Higher annual fees and setup costs

Third-party dependency can result in delays and increased risk

Lower interchange revenue

No matter if you choose a processor-only or program-managed setup, multiple parties need to be tied together to get your card program up and running.

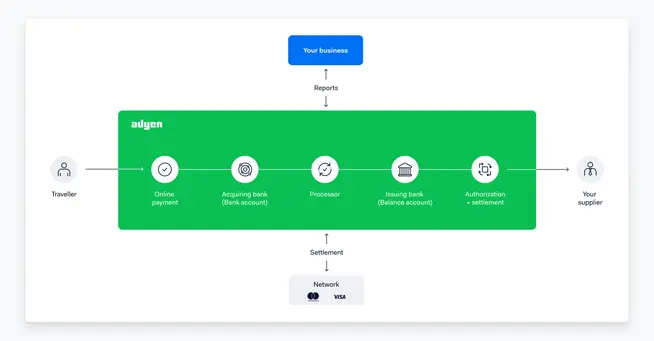

True end-to-end payments setup

The providers that offer issuing and acquiring in one solution rely on third parties for banking licenses. They build a layer of technology that aggregates all elements of a payment setup and sell it as an end-to-end solution. Unlike these aggregator providers, we own all the technology and licenses at Adyen and are the only provider globally to offer a true end-to-end payment setup.

A true end-to-end payment setup means that we’re a fully licensed provider for issuing and acquiring. We build everything from the ground up, eliminating the need for complex, multi-party setups, lines of credit, and high working capital. By combining issuing and acquiring in one platform, your incoming funds will be instantly available for virtual card payouts.

Are you ready to take your supplier payments to the next level?

If you're using virtual cards to automatically and securely deliver funds to your suppliers, you’re perfectly positioned to take the next step in supplier payments.

This is a new way of enhancing your virtual card setup that speeds up cash flow, reduces risk, and allows you to invest more in your business.

Transforming your issuing setup is also a way to open up new revenue streams. When a card transaction is processed in our issuing program, we share the interchange revenue with you.

Partnering with Adyen means you only need one integration for a complete end-to-end setup and don’t have to worry about licensing or local compliance in terms of technology.

Our in-house built platform and banking and acquiring licenses give us control of the full value chain, increase the speed of innovation, and improve flexibility since we don’t depend on external parties.

Get started with a new way of doing issuing here.