Podcasts

Marginal gains #2: Processing payments

In part 2 of our Marginal Gains series, we’re heading to the beating heart of the payment journey: processing payments.

Navigating the global payments landscape is like riding a mountain stage of the Tour de France. It’s unforgiving for the uninitiated, awash with complexity, and can be even harder to maneuver when you’re hindered by out-of-date technology.

Today, there are many different ways for businesses to send a payment to an issuing bank, and each of these issuing banks has its own tech platforms and procedures. Payment providers, in turn, have been unable to keep up with the technology available for consumers, making the road to success a bumpy, uphill battle for many businesses.

In recent years, we’ve seen massive strides in how payments are processed. In this article, we’re going to take a look at some effective ways to boost your processing and the products Adyen offers to help. Now it’s time to change gears.

Étape 1: Get the best route for processing payments with local acquiring

Modern global businesses span continents, have numerous distribution channels, suppliers, and even offices. Amidst this complexity, the best solution foraccepting paymentsis often found by working alongside one partner with local acquiring licenses for all the markets in which you operate.

How local acquiring can get you ahead of the pack

Payments processed using local acquiring often cost less and are more likely to be authorised. At Adyen, our local acquiring connections are centralised, so we can view payments across all regions and channels in the same place. By using our acquiring, you can track payment methods, performance, spot trends, and get to know your loyal customers.

Using Adyen for acquiring also means access to RevenueAccelerate and its features, including Network Token Optimisation.

"Having leveraged Adyen’s local acquiring solution in other markets, we are excited to enjoy the same benefits in Malaysia including a more than 3% increase in authorisation rates.”

Étape 2: Power your processing payments with performance-enhancing Network Tokens

Saving payment card details is revolutionising how we pay online.

Network Tokens are a secure card token from EMVCo, replacing the card number (PAN) for payments. They were originally developed to maintain security while preventing payment disruption when it came to card expiry. They're maintained by card networks, available in upwards of 150 countries, and automatically updated when a shopper's card details change. This, and the use of Adyen’s Account Updater, offers a simple way for businesses to access up-to-date card information in real-time.

Network Tokens are out ofPCIscope, so merchants can operate with these tokens without the need to be PCI compliant.

Benefits of Network Tokens

Using Network Tokens can give you higher authorisation rates and deliver shoppers an uninterrupted service even when their payment details expire. Adyen data shows that 10% of cards are refused because of card expiry, or by being lost or stolen. Network Tokens stay the same while the network updates the card details, meaning uninterrupted billing for cardholders and no need for merchants to update the token they store.

Because of the improved security built into the technology, issuers trust Network Tokens. This means a greater likelihood of an accepted payment when a Network Token is used. To top it all off, that elusive 10% goes back to your revenue, slightly more than a marginal gain.

New technology to solve old problems

Network Tokens are a recent innovation, built with the goal of replacing account numbers in the not-so-distant-future. In the long term, businesses may be able to skip the costly and time-intensive PCI certification, freeing up time to focus on what they're good at.

Despite their obvious benefits, issuing banks can be apprehensive when implementing Network Tokens. Issuers need to build the capability to approve Network Tokenized transactions, meaning that while some markets see a high number of issuers building with tokens in mind, some aren't ready. Additionally, not all issuers authorise Network Tokens on par with PAN authorisations, so there's potential for a drop in authorisation rates if an intelligent approach to routing isn't applied. Fear not though, this is where Network Token optimisation comes in.

Why Network Token Optimisation is needed

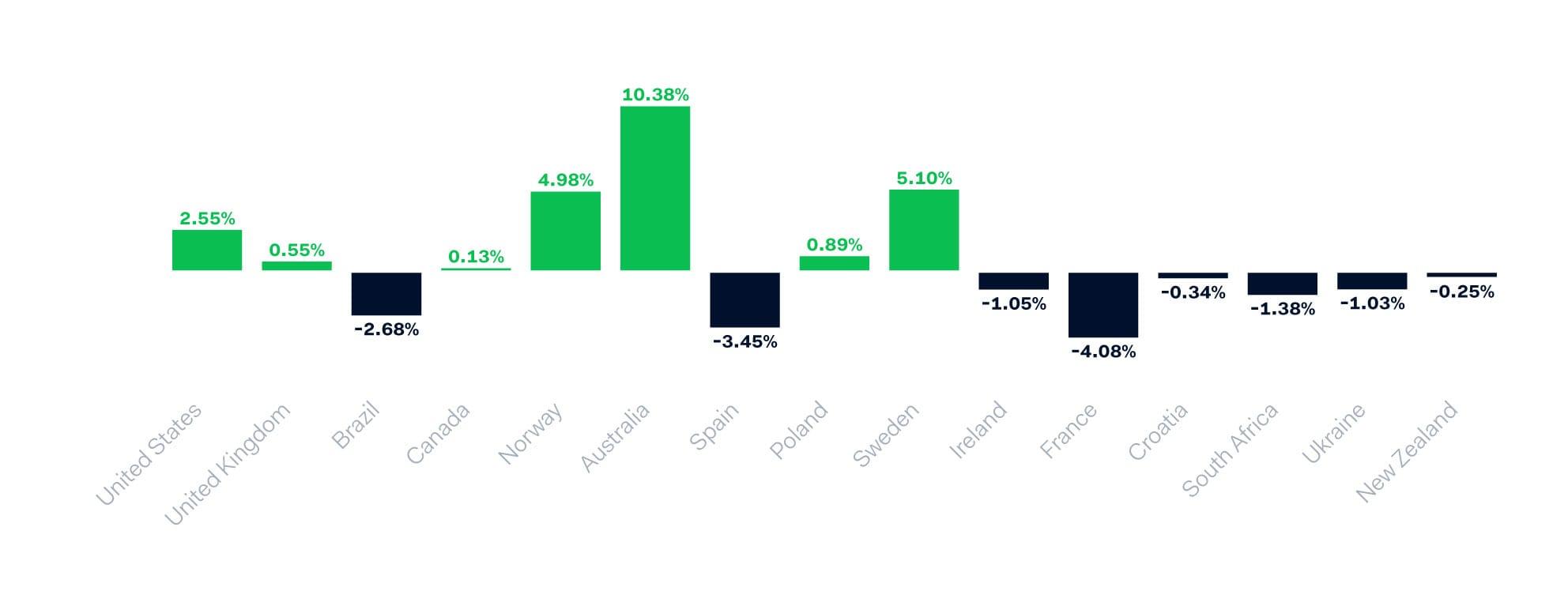

In the chart below, we show Network Token adoption across different regions and the uplift (or decrease) in authorisation rates they bring. Sweden is a case in point. With the country’s propensity to prefer cashless payment methods, authorisation rates increase by 7% if you offer Network Tokens with intelligent routing. Look at the UK however, and you see a smaller increase.

Network Token adoption across different regions

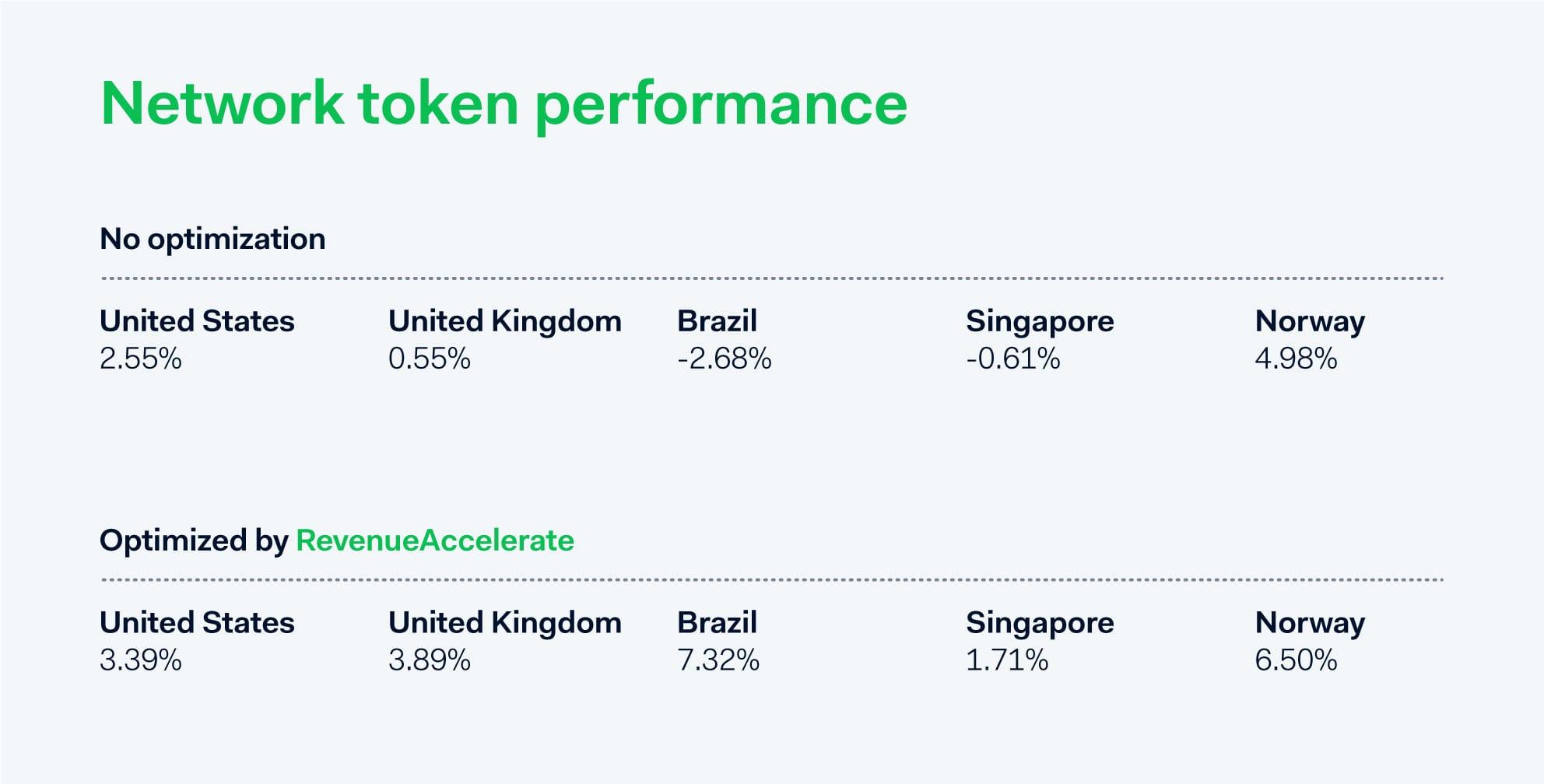

This isn’t the full story though. While illustrating a small 0.55% increase across payments in the UK, the chart below also shows that the issuing banks utilising Network Tokens are experiencing great uplift.

Network token performance in the UK

With Network Token Optimisation, we can decide when to use a Network Token versus a PAN, based on our machine learning capabilities and platform data. We only send Network Tokens if it’s the issuer’s preference, and even if the shopper’s card is declined, we can immediately retry with the PAN.

We're already seeing impressive results using Network Token Optimisation:

Étape 3: Smart Payment Messaging for the fastest finish

Consumers have long borne the brunt of all the crossed wires and confusion that surround processing payments. Time and time again they’ve seen their checkouts interrupted, subscriptions terminated, and payments incorrectly blocked. What this calls for is a continuously learning engine that modifies payment messages to each issuer's liking.

Smart Payment Messaging is a feature of our payment experience tool, RevenueAccelerate that allows us to adapt the format of payment messages to best suit an issuing bank’s preferences.

We automatically reformat the data sent with each payment request according to the issuing bank's specific preferences and past behavior. This could be in the form of a card expiry date or a shopper's address. Smart Payment Messaging is at its most effective in complex payment environments or where outdated issuing banks are prevalent.

The best fit for new regulations

When banks don't update to incorporate the latest card network regulations, things can get complex. We saw this happen with the introduction of new card-on-file indicators by Visa and MasterCard in 2018. Some banks neglected these updates, leading to a significant number of declined payments. Smart Payment Messaging can mitigate this by recognising changes and adapting the payment message to the old format for such banks, leading to approved payments and happy shoppers.

Other banks have non-standard behaviour when it comes to receiving authentication data. In 2020, a new regulatory requirement meant that data needed to be sent in a different way to banks; in a slightly different place in the payment message; yes it can get that complicated. Some banks haven't adapted to this yet, and again we've discovered Smart Payment Messaging racing to the rescue.

How payment messaging can sustain your growth journey

Issuers decide to approve or decline a payment based on the data contained in payment messages. Tweaking these messages can be the difference between a happy customer, and one that never returns.

Nevertheless, as issuers' preferences change, so does our Smart Payment Messaging. This means that authorisation rates stay up even if an issuer turns its system upside down.

Out of the mountains and onto the track

The hard part is over; you’ve learned what’s on offer when it comes to processing payments. So whether it’s with messaging, acquiring, or Network Tokens, make sure you’re using what’s available to make those marginal gains.

For our next article in the series, we’ll be talking about protecting shoppers: improving security with risk tools while nailing the customer experience.