Article

Interchange fees explained

This 2026 article explains how interchange rates work across credit and debit cards, and how they vary by region.

Understanding interchange fees is necessary for compliance. On top of that, businesses can improve margins by reducing fees when possible. As payment ecosystems evolve in 2026, businesses that actively manage these costs will have a clear advantage.

In this article, we'll walk you through the factors that impact interchange fees, where to find the most up-to-date interchange rates, and the opportunities to reduce them.

This article includes:

What are interchange fees?

How much are interchange fees in 2026?

How interchange fees work

What fees make up card processing?

Where to find current interchange rates

How interchange fees are calculated

Can you reduce interchange fees?

Interchange++ vs blended pricing

Interchange fee regulation

What are interchange fees?

Interchange fees are charges that an acquiring bank pays to the cardholder’s bank every time a customer pays with a card. The business then pays the interchange fee back as part of its card processing fees.

Card networks like Visa and Mastercard set the interchange fees. These make up the largest portion of card processing costs.

What is interchange revenue?

Interchange revenue is a way for businesses to earn a share of the fees made from card transactions made using cards they issue. With embedded finance, companies can build tailored, global card programmes that offer physical or virtual cards that let users receive and spend funds almost instantly. Each time a payment is processed, the issuing bank shares a portion of the interchange fee with the business, creating a new and scalable revenue stream.

How much are interchange fees in 2026?

Interchange fees in Europe (EEA) & the UK

Debit cards: ~0.2%

Credit cards: ~0.3%

Interchange fees in the United States

Typically 1.5% to 3.5%+

Key insight: Europe remains one of the cheapest regions globally due to regulatory constraints, including in markets like Sweden.

Where to find current interchange rates

Interchange fees are usually a percentage of the transaction amount. Many factors influence what this percentage is.

You can find the most up-to-date interchange rates directly from the card networks:

Card schemes set interchange fees and are non-negotiable. They are also regularly adjusted. Visa and Mastercard publish new rates in April and October every year. You can find the most accurate and up-to-date rates on the card scheme’s website.

Some card networks, including American Express and Discover, work slightly differently from Visa and Mastercard and don’t publish their rates online.

How interchange fees work

There are three main parties involved in the payment process:

Issuing bank: The customer’s bank that provides the card

Acquiring bank: The customer’s bank that processes the payment

Card network: The system (like Visa or Mastercard) that connects the two

When a customer pays with a card, the payment is sent through the card network to the issuing bank for authorisation. Once approved, the merchant receives the funds without processing fees.

A portion of these fees (the interchange fee) is paid to the issuing bank. This fee compensates the bank for issuing the card and handling the transaction.

In short:

A customer pays with a card

The merchant receives funds (minus fees)

The issuing bank earns the interchange fee

What fees make up card processing?

There are three main components:

Acquirer markup: Charged by your payment provider

Scheme fees: Charged by card networks

Interchange fee: Paid to the issuing bank and typically the largest cost component

How interchange fees are calculated

Interchange fees are usually a percentage of the transaction. The exact rate depends on multiple variables.

Key factors affecting interchange:

Here's a breakdown of the key factors to be aware of and how they affect the amount you pay:

Card scheme: Different card schemes charge different interchange rates. So the cost of a customer paying with a Visa card won't be the same as with a Mastercard.

Transaction type

Card-present (in person): Lower fees

Card-not-present (online): Higher fees (more risk of fraud)

Card type: Credit and deferred debit cards have higher interchange fees than immediate debit and prepaid cards, as the level of risk is considered higher.

Debit cards → lower fees

Credit cards → higher fees

Merchant category code (MCC): Certain industries may qualify for lower rates. For example, in the US and Australia, Visa and Mastercard offer lower rates to businesses such as charities, travel agents, streaming services, and utilities.

Consumer vs commercial cards: Commercial cards charge higher interchange fees than consumer cards.

Transaction location: Domestic transactions, where the card-issuing bank is in the same country as the business, are generally cheaper than cross-border transactions.

Domestic → cheaper

Cross-border → more expensive

Rewards cards: If a customer uses a rewards card to pay, the interchange fees are generally higher. This is because the increased fees pay for the extras offered by rewards programmes.

Can you reduce interchange fees?

You can reduce interchange fees by optimizing your payments. There are certain aspects you can influence to reduce costs. For instance, interchange fees for in-person payments are lower than for online payments. By selling more in store, you could reduce your interchange fees.

You can also reduce interchange fees through enhanced scheme data (ESD). ESD is additional payment data about your customers’ purchases that you can send to the card scheme with your payments or capture requests to qualify for lower interchange fees. The card scheme then sends this data to the shopper’s bank so the shopper can access all the data in their transaction statement.

What you can influence:

Encourage debit payments

Reduce fraud risk

Use local acquiring

Enhanced scheme data

Optimise checkout flows

What you can’t control:

Card network pricing

Assigned MCC

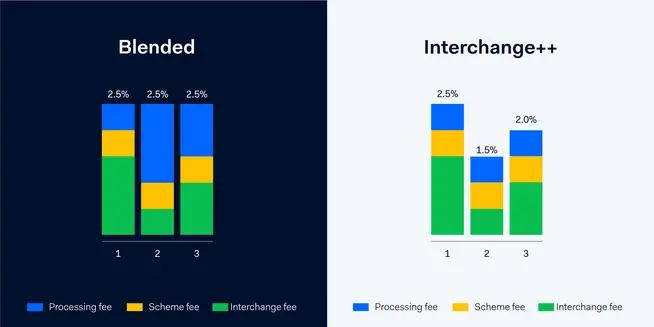

Interchange++ vs blended pricing

Interchange++ and Blended are the most used pricing models for card transactions. The main difference between them is transparency.

Interchange++ provides a detailed breakdown of the three payment card costs mentioned earlier: the acquirer markup, the card scheme fee, and the interchange fee.

You only pay the interchange fee the card issuer actually charged you. As interchange fees vary depending on many factors, they can sometimes be lower than a fixed rate.

The alternative to Interchange++ is Blended pricing. The Blended model charges an average processing cost plus a fixed markup. You're charged the same markup on every transaction, and you can't see the cost split.

While a fixed fee may seem easy to understand, it's not transparent.

Interchange++

Transparent breakdown of fees

You pay actual interchange + markup

Can be cheaper over time

Blended pricing

Fixed rate per transaction

Simpler, but less transparent

Savings from lower interchange fees are often hidden

Interchange fee regulation

Traditionally, there was very little transparency into how interchange fees were calculated. Large businesses with high transaction volumes could negotiate lower fees, while smaller firms had to pay the full amount.

Regulators and card networks have recently taken steps to standardise interchange fees by introducing stricter rules, fee caps, and greater transparency.

The following are regulations that shape global interchange fees.

European Interchange Fee Regulation (IFR)

The European Economic Area (EEA) introduced interchange fee regulations in 2015. This led to heavy interchange fee regulations, capping interchange fees for consumer cards across all countries in the EEA. As a result, the EEA is now one of the cheapest options worldwide and is considered an excellent place to set up entities for cross-border transactions.

Since the UK's withdrawal from the EU, the EEA fee caps no longer apply to transactions when a customer uses an EEA-issued card to pay at a merchant in the UK, or when they use a UK-issued card to pay at a merchant in the EEA.

The interregional caps apply to transactions at merchants located in the EEA and the UK. The EEA and UK interregional fee caps for card-present transactions are 0.20% for debit transactions and 0.30% for credit transactions. For card-not-present transactions, the fee caps are 1.15% for debit transactions and 1.50% for credit transactions.

US: The Durbin Amendment

The Durbin Amendment, introduced in 2010, caps debit card interchange fees for large banks and requires competition between card networks. Its goal is to lower payment processing costs for merchants.

The Durbin amendment is dependent on the size of the issuing bank's assets. If the issuing bank has assets of $10bn or more, its debit and prepaid cards will be charged regulated rates. These cards are then subject to an interchange rate of 0.05% + $0.21 or 0.05% + $0.22, depending on fraud prevention policies.

Key takeaways

Interchange fees are the largest cost in card payments

They are regulated in Europe but market-driven elsewhere

You can optimise but not eliminate them

Choosing the right pricing model has a major impact

Ready to optimise your card program and maximise interchange revenue? Get in touch today to learn how your business can benefit.

Interchange fees FAQ

No. They are set by the card networks (like Visa and Mastercard) and are charged by the customer's bank (the issuer). These rates are non-negotiable and change periodically based on market regulations and network updates.

However, businesses can optimise their costs by using local acquiring to benefit from regional fee incentives or by implementing security tools like Address Verification Service (AVS) that can trigger lower interchange categories.