Article

Modern card issuing to enhance your card programme

Discover how modern card issuing can help B2B payments on enterprise businesses and platforms and how you can enhance your card programme with Adyen end-to-end setup.

Modern card issuing is growing in popularity as B2B enterprise companies are looking for new ways to optimise payments. With commercial card programs you can now optimise payouts, control risk and increase your revenue.

Thanks to a flexible API-driven approach, modern card issuers offer a clear path to harnessing the benefits of a card program compared to traditional banks. However, many issuers have multiple third-party dependencies, adding risk to your card program.

In this article we aim to guide you through the advantages of modern card issuing, which can be relevant for expense management, supplier payments, and SaaS platforms. We'll deep dive in the current limitations and how end-to-end card issuing platforms can overcome most of these struggles.

Differences between traditional and modern card issuing

Card payments came into the scene as an alternative for cash payments. However, they quickly expanded beyond business-to-consumer (B2C) into the B2B landscape as an effective option to facilitate large-scale transactions.

How did this happened? Let's take a look back.

Challenges with legacy solutions

Card issuing technology was first developed by traditional banks for their own use, but because of this internal usage, card issuing solutions weren't seamlessly integrated with others.

Although banks had the necessary licenses and network memberships to support card issuing, integrating their legacy technology with businesses' infrastructure took a lot of work. This resulted in time-consuming and inflexible setup processes, with limited room for customising the card programs to businesses' specific needs.

Modernising card issuing with added technology

With the goal of making the process smoother modern card issuing solutions aim to make card programmes more accessible through an extra layer of technology. This technology allows new card issuers to communicate with banks and network infrastructures through APIs.

The API-led approach to card issuing has multiple benefits:

Reducing implementation times

Ad-hoc customisation of card programmes that align with each business needs. Organisations can pick and choose which features they want to use and easily add them through API calls.

Modern card issuing to revolutionise the industry

Modern card issuing brings several benefits to business and end customers. Let’s review the ones that can bring more value.

Quick to adopt and deploy

A model based on API allows businesses to deploy card issuing solutions faster than previous approaches. Reducing implementation times will help your business to have its customised card programme running in no time. And as they say, time is money.

If you want to gain even more speed, you can skip the process of approving and manufacturing physical cards by launching a digital-only card program.

C ustomise and personalise

Modern card issuing platforms offer a full range of customisation and personalisation options so your cards can be tailored to your needs. Thanks to flexible APIs your card programme will meet all your unique requirements.

Whether you prefer to issue physical cards with your branding or provide virtual cards for added convenience, the choice is yours.

Increase revenue

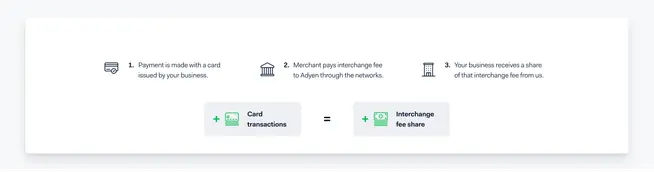

New card issuing solutions aren't just about improving UX or streamlining payments; it's also a powerful tool for maximising revenue by opening up new revenue streams. You receive a share of the interchange fee for every card transaction processed through your issuing program. This can boost your finances by transforming your payment operations from a cost centre into a revenue driver, helping your business grow in the competitive landscape.

Modern card issuing - how businesses use it today

Businesses use card issuing for various cases. While it's proved itself to be valuable, it also has its limits.

A new way of issuing cards has emerged as an innovative solution to these limitations. Before diving into this, let’s review how businesses use modern card issuing today and what challenges they face.

Managing expenses

As an expense management provider, you offer a solution that streamlines the expense process for businesses. This means eliminating as much of the error-prove manual work as possible, like submitting, reviewing, and approving expenses.

By adding cards to your offering, your customers can issue cards to their employees for business expenses. They can control spending limits for amounts, merchant types, and locations. The need to manually submit and approve expenses is gone. An automated process reduces disputes and errors.

But, with most modern card issuers, you still need to deal with third parties. Whether direct or indirect, you can end up with various integrations and agreements with third parties like banks, KYC providers, and risk management solutions. This creates unnecessary complexity. And it can again result in an increased risk of errors, slower speed to market, and difficulty in ensuring the same experience everywhere.

Paying suppliers

If your business needs to pay suppliers on a large scale, you know how important fast and reliable payouts are. With modern card issuing, you can make the payout process more efficient, while ensuring your suppliers always get their money on time by taking advantage from virtual cards.

Take an online travel agency (OTA) as an example. They have multiple hotels, activities, and transport options connected to its platform. The user experience for travellers who book and pay through the platform is great. But making sure that the international hotels and airlines receive their money fast is a challenge.

Modern card issuing can solve this. With virtual cards, you can provide a reliable and automated solution for instant supplier payments. But, because the incoming and outgoing funds are decoupled (as they're handled by separate acquiring and issuing banks), you'll need high working capital or lines of credit.

Embedded finance

As a SaaS platform, you're empowering businesses, such as beauty salons or restaurants, with essential tools to run their operations. Your software helps them manage their bookings, do accounting, and invoicing. For a fully comprehensive solution, your customers also need financial services.

Platforms that have embedded payments into their offering remove much of the friction regarding payment acceptance for small businesses. They create a solid foundation to expand into the next frontier of exceeding their users' expectations: embedded finance.

Integrating financial services into your platform can make fund movement a lot faster. By embedding money management accounts into your platform, you make incoming funds accessible for users straight away.

With card issuing, your users can spend their earnings using platform-issued cards instantly, bypassing the need to wait for transfers to their external business bank accounts.

Currently, not many providers exist that offer an embedded finance suite, but those who do deal with the same dependencies as mentioned before. Since they don't own the right licences, they are limited by third-party restrictions in how businesses can offer these financial products to their customers.

Want to dive deeper into the opportunity embedded finance presents to platforms? Check out our BCG report.

''Modern card issuing has streamlined B2B payments in sectors like online travel, SaaS, and expense management. However, we see a growing demand with enterprise businesses for an all-round solution.''

George Smith

Global Head of Strategy, Adyen Issuing

The next stage: end-to-end card issuing

Setting up a card programme has been made much easier and more accessible with modern card issuing. But, these solutions are still built on legacy infrastructures, dependent on multiple providers. This makes puts them at risk of slow innovation, opaque pricing, high chance of errors, and delays in cash flow.

You can avoid these issues by using an issuing partner that owns both the technology and the right banking licences.

A true end-to-end card issuing solution with our single financial technology platform

Adyen Issuing is the first true end-to-end issuing solution. We've built it in-house for enterprise businesses and have our own banking licences. We provide the same flexible API-driven technology that modern card issuers provide, making the integration and management of card programs fast and flexible.

This unique combination of owning our technology and banking licenses eliminates the need for third parties, allowing our customers to experience the benefits of modern card issuing with added speed and stability.

A technology provider, acquirer, and issuer in one

Since we're a fully licenced acquiring and issuing bank in the EU, UK, and US, we can combine issuing and acquiring within a single platform. This lets businesses make incoming funds instantly available for supplier payments to issued cards. Which minimises the reliance on high working capital or lines of credit. Businesses can benefit from virtual card payments without the delays caused by a fragmented setup.

Because we don't rely on third parties, we also have the freedom to drive innovation at our own pace. As we have control over our entire infrastructure, we can align our solution with the evolving needs of our customers.

Scale across markets from the same integration

If you’re an expense management company or SaaS platform, you can manage all card programs through the same platform and offer the same experience everywhere. With our end-to-end card issuing solution, you can enjoy all the benefits of a global card program with just one single integration, one provider, and one contract. You can rely on us to help craft a card program that meets your needs and lets you focus on your core business.

Our platform lets you expand your card programme to different markets through the same integration, eliminating the complexity of finding new partners in every market. You don't have to worry about local regulations as our technology meets compliance in the markets we operate.

Transparent pricing

As we own the entire value chain and don't depend on third parties, scheme fees are the only external fees included in our pricing. We have complete control over our pricing, making it transparent and static, in contrast to the vague and dynamic pricing determined by third parties.

The model we use for pricing is called interchange - -. As our pricing is transparent, the interchange fee share you'll get is predictable.

''Our issuing solution gives you all the benefits of running a card program without having to deal with its complexities. It's our unique end-to-end approach which makes this possible.''

Willem van Driel

Head of Issuing Product, Adyen

Are you ready to take the next step in card issuing?

With Adyen's end-to-end card issuing solution, you can your payment setup to new heights.

Our platform and banking and acquiring licences provide total control and unparalleled flexibility. Say goodbye to complex, third-party dependencies and hello to a complete, seamless solution.

Interested in learning more about how Adyen can help you elevate your issuing strategy? Reach out to us and we’ll help you with all your questions.