Reports

Kenya and the original mobile payment service

We look at Kenya's payments landscape, its position as a tech hub and how the region embraced M-Pesa

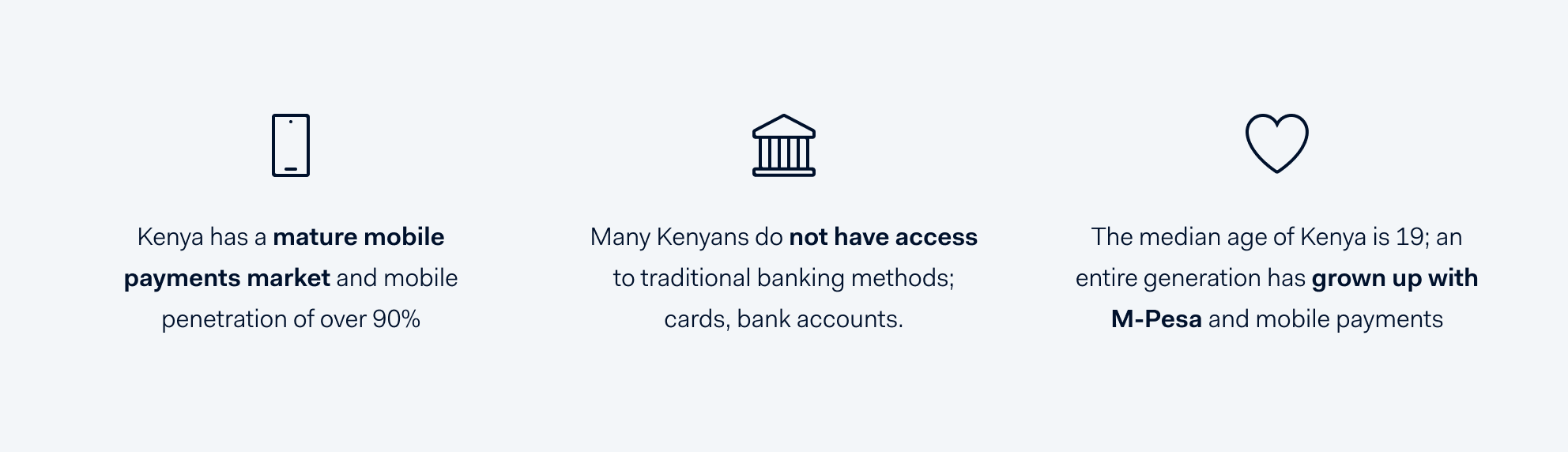

Kenya is a country of contrasts. It has a population of only 48 million yet it is home to 68 languages. It's renowned for its wildlife and nature, yet it's home to some of the most densely populated cities in Africa. It has a large percentage of unbanked citizens, yet it has one of the most mature electronic payment methods in the world.

When Facebook CEO Mark Zuckerberg visited Nairobi in 2016, he declared Kenya a “world leader” in mobile money. This is in no small-part down to M-Pesa, the original mobile payment service. According to pymnts.com,“sub-Saharan Africa accounts for 49 percent of all mobile money accounts globally, with use especially high in eastern Africa, a region that includes Kenya, Uganda, Rwanda and Tanzania”.

With its mature market of mobile payments and a growing ecommerce sector, now is the time for businesses to expand their offering into Africa. We’re excited to be among the first global payment service providers (PSPs) to go live in Kenya and offer M-Pesa.

Key points when considering Kenya

The story of M-Pesa

Paying bills online, without the need to queue outside a bank or post office is something many of us take for granted, yet until recent years, this wasn't possible for many Kenyans. A high rural population, paired with limited transportation networks meant that for many, arduous journeys to towns and cities were required in order to perform simple banking tasks. M-Pesa changed that with its easy to use SMS based service.

Since 2007 M-Pesa has allowed users to pay for goods and services, as well as transfer and save money. Initially developed to help small businesses repay microloans usingSafaricom’snetwork, it became indispensable to the rural population and Kenya's economy on the whole. As an example, cash carrying bus drivers quickly discovered that accepting M-Pesa was a safe way to avoid the high percentage of counterfeit bank notes in circulation.

It soon became more than a payment method. Instead, a sign of tech emergence and growth on the continent as a whole. Kenya bypassed the desktop banking era and leapt ahead of the curve; Europe and North America are still playing catch-up.

The Silicon Savannah

The success of M-Pesa has led tech's major players like Zuckerberg to look towards Africa for the next wave of innovators. According to Quartz Africa, start up investment in Africa increased 400% in 2018, with Kenya attracting the third highest investment after South Africa and Nigeria.

With such high investment and opportunity, many African cities are staking their claim to 'The Silicon Savannah' tag. Like Silicon Valley in the US, The Silicon Savannah is used to describe an area with a burgeoning startup and technology infrastructure. In Africa, this applies to mega-cities like Lagos, Johannesburg and Nairobi.

Aside from boasting the original mobile payment method, Kenya's Silicon Savannah is greatly aided by superior internet connectivity compared with the rest of the continent. In 2009 a submarine fibre-optic undersea cable called The East African Marine System(TEAMS) was developed to connect East Africa with the rest of the world. Now, the size and scope of Africa along with its vastly improving infrastructure means that it is a continent in which many global businesses will look to expand.

Kenya’s Payment Makeup

Unsurprisingly, Kenyans are big fans of mobile money. 90.4% of Kenya's population has a smartphone, and approximately 50% use them to make payments. Debit and credit cards have low penetration though and there is still a significant population of citizens without traditional banking facilities.

Payments in action

Our Local Payments Manager Willemijn recalls how M-Pesa came to her rescue while traveling through East Africa:

“Back in 2013 my partner and I were travelling in the far west of Kenya, in a beautiful rural setting with a few small villages. While enjoying the surroundings we noticed we were fast running out of gas and, even worse, had no cash. It was stressful to say the least!

We drove between the three nearest villages, but to our horror, none of them had an ATM. We were getting desperate and called a friend a few hundred kilometres away in Nairobi. He didn’t share our anxiety. 'Don’t worry, just use M-Pesa' he said, and told us to look for an M-Pesa agent. It turned out that these were everywhere. Every shack and general store hosted this payment method. My friend sent money to our Kenyan phone number, we presented the reference number in-store and they handed over the cash. Crisis averted.

I loved my visit to Kenya so much, and my experience with M-Pesa, so when the opportunity came to work within the African payments landscape, I jumped at the chance. I’m now looking forward to helping businesses expand their payment offerings in the continent, starting with Kenya.”

What Adyen offers

We can take you to key African marketsKenya, Uganda, Tanzania and Ghana with a single integration and no extra contracts. We also operate in South Africa and Nigeria as a payment gateway.

We're working with local PSP Cellulant to make it easy for your business to accept mobile payment methods in several African countries. Cellulant processes 12% of Africa’s digital payments today and is the mobile banking and mobile payments provider to 120 banks in Africa.

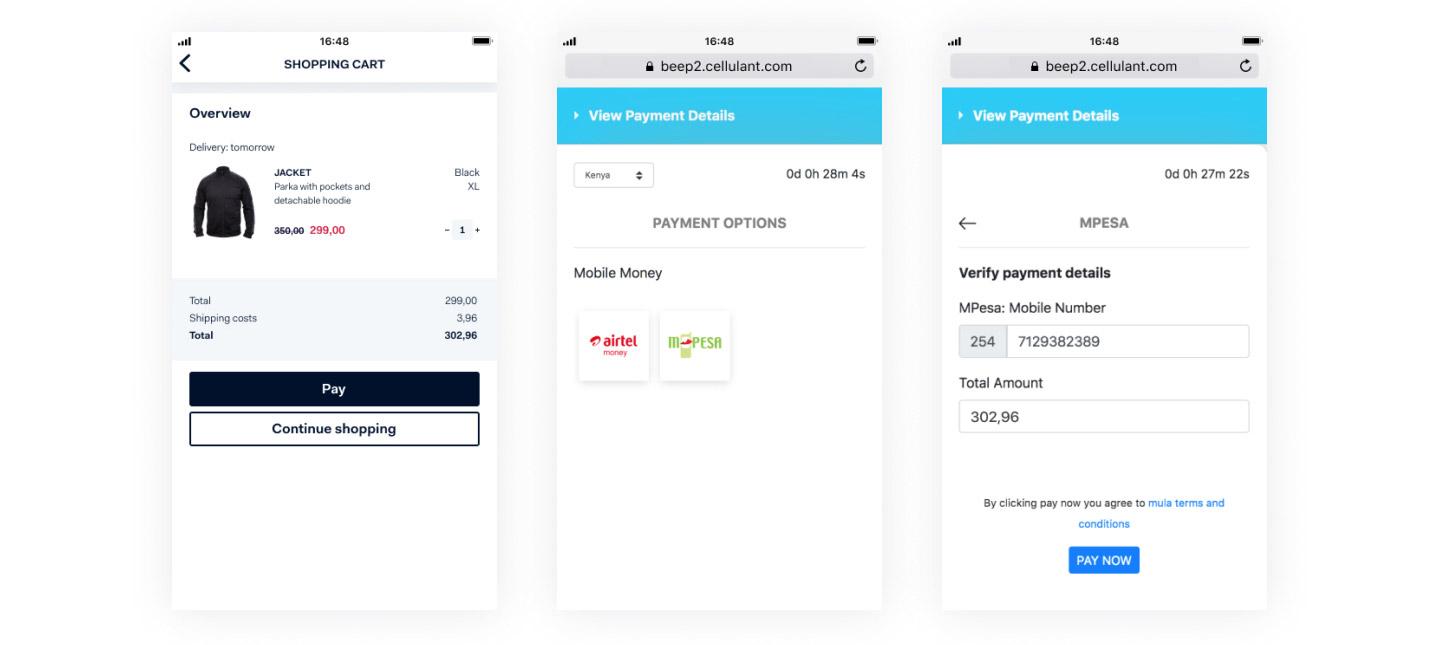

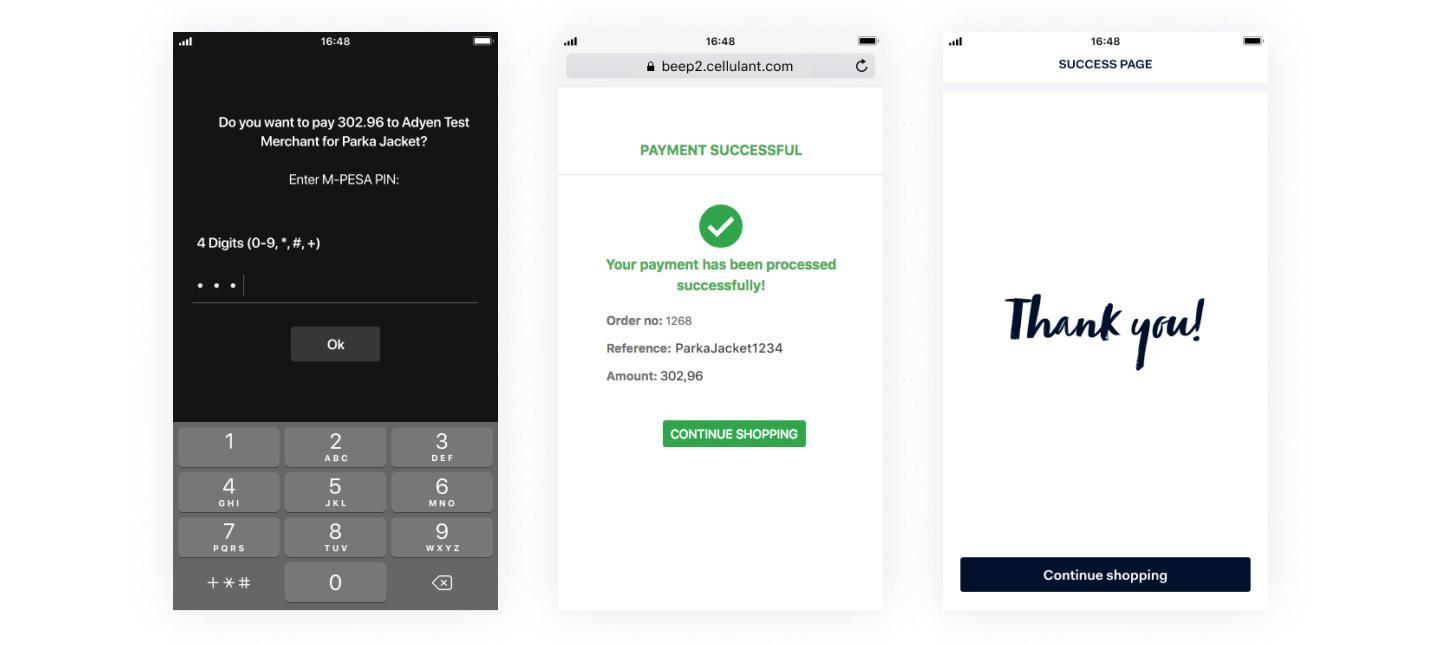

Payment flow

The payment flow for M-Pesa is simple and effective. From shopping cart to 'success', users can make individual or split payments in 4 easy steps:

For split payments, a push notification is sent with a reference code and a configurable payment deadline. This makes sure that payment is made and everyone has chipped in their agreed amount. For example, if a family needs to collectively pool resources for a large purchase, they can. A common use case for this is booking flights.

Doing business in Kenya?

The Silicon Savannah is calling. With record levels of investment and a fast-growing tech infrastructure, it's a great time to grow your business in Africa. Want to find out more?Get in touch.