Reports

Go global with local acquiring

How to optimise your cross-border transactions while keeping things simple with one acquirer.

Are you planning on expanding cross-border? Or perhaps you’re already selling in several markets but want to streamline your cross-border payments?

Either way, read on.

Global commerce is no longer reserved for large businesses. Today, thanks to tehnology companies like Adyen, pretty much any business can accept and reconcile payments across borders with minimum fuss. And, if you process card payments (which you probably do), acquiring plays a big part in this.

What is local acquiring?

You wouldn’t be the first to ask. To help you out, we made this video that explains acquiring in less than 55 seconds:

An acquirer is a bank that processes credit and debit card payments on behalf of a business. It sends purchase authorisation requests via card networks (like Visa and Mastercard) to the customer’s bank. It then either brings you the money or tells you why the request has been declined.

So far so easy.

Processing cross-border payments

It begins to get a bit complicated when you’re processing cross-border transactions. Suddenly you have some choices to make:

- Do you want to process using a cross-border approach where one central entity in one country accepts cards in multiple countries via a single acquirer?

- Or would you prefer to take a local approach where your local entities have a card acceptance contract with a local acquirer or an international acquirer with the relevant domestic licenses?

Or maybe you have no idea. Let’s break it down:

Cross-border vs local acquiring

To illustrate the difference between cross-border and local acquiring, here’s a scenario:

You’re a UK-based business. A Spanish shopper is attempting to buy something from your ecommerce site. The shopper enters their credit card details and hits ‘pay’.

What happens to cross-border transactions:

Your UK-based acquirer approaches the customer’s bank in Spain and requests the authorisation of the transaction. There’s no need to set up a local entity in Spain; the whole thing is managed out of the UK with a single partner and one set of reporting.

Nice and simple, but of course there’s a catch.

The Spanish bank might not be familiar with this UK acquirer. And perhaps the authorisation request message contains data that the bank does not recognise. On top of that, maybe there's been a recent surge in cross-border fraud from the UK. The bank errs on the side of caution and the request is refused.

(That isn’t to say, of course, that every cross-border transaction would be declined. But it is more common for the reasons illustrated above.)

What happens to local transactions:

In this case, when your Spanish shopper hits ‘pay’, your local, Spanish acquirer approaches the Spanish bank with an authorisation request. The request is not only seen as local but it’s perfectly formatted to meet the specific requirements of that bank. The bank allows the payment to proceed, the acquirer releases the funds and your sale goes through.

"Through local acquiring, we were able to reduce our bank declines by 21%"

So, locally processed transactions tend to generate higher authorisation rates than cross-border transactions. But let’s take a look at what’s going on under the hood.

You’ve got a local acquirer in Spain and a local acquirer in the UK - that’s two acquirers at least. And what if you’re selling in France and Germany as well? Or have plans to expand to the US? That’s potentially five acquirers with five contracts, five service level agreements, and five sets of functionalities. Each one has its own set of reporting with different formats and data elements making reconciliation increasingly complicated. Add a few local payment methods into the mix, throw in some extra channels, such as in-app or physical stores, and your head is starting to spin.

There’s got to be a better way.

Local acquiring with one global partner (aka 'the sweet spot')

The best solution is to have a single partner with local acquiring licenses in all the markets in which you operate. That way, you can benefit from higher authorisation rates, lower transaction fees, and faster settlement in each market. You’ll also enjoy the simplicity of just having one partner to deal with. This not only makes reconciliation a breeze. You’ll be able to view all transactions from across all regions, channels, and payment methods in the same place. So you can track performance, spot trends, and get to know your loyal customers.

Adyen has local acquiring licenses across Europe, North America (including Canada), Brazil, Hong Kong, Australia, New Zealand, and Singapore. And we’re adding new licenses all the time. Where we don’t have licenses yet, we team up with local partners to ensure you still get the benefits of processing locally. So, wherever you are, and wherever you want to be, we have you covered.

With us, you can also support local card networks such asCartes Bancairesin France and Interac in Canada. And local customers can pay however they like thanks to our support of all major local payment methods. No need for separate agreements or technical integrations these methods can be added with the flick of a switch.

"Adyen helped us with local acquiring in the US, which had a positive effect not only on our top line but also on the bottom line. Through local acquiring, we were able to reduce our bank declines by 21%." - Dennis Friemerding, Team lead payments, FlixBus

Boosting your settlement performance

Another important consideration when you’re processing cross-border payments is how money is settled into your account. Ideally, you want to get paid as quickly as possible in whichever currency you prefer. Adyen has extensive global coverage of over 30 currencies. So you know you’ll be paid in the currency you want.

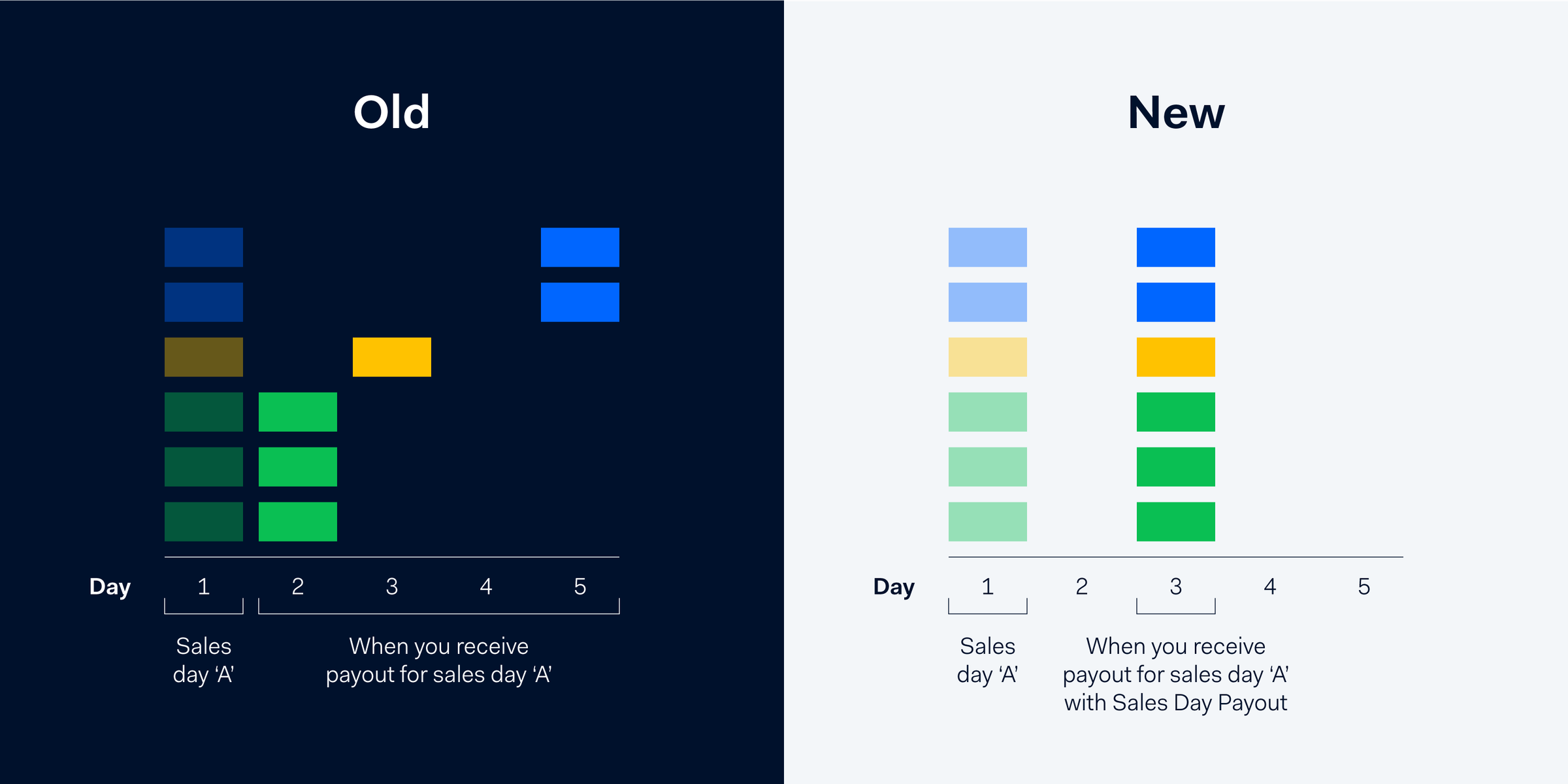

Sales Day Payouts

To make sure you're paid-out quickly and predictably, we’ve recently switched to Sales Day Payout. With this payout method, you’ll be paid a full sales day all in one go, regardless of whether we've received the funds from the card or payment providers. This simplifies the reconciliation process it allows for predictable cash flows.

Below, you can see the benefits of Sales Day Payout vs the old Pass-Through method. All this is made possible thanks to our banking license.

Better billing with Interchange++

Another important consideration when processing card payments, is how you're billed for each transaction. Not all billing models were created equal. Adyen bills using Interchange++ rather than a Blended rate, but why?

With a Blended rate, you pay an average processing cost plus a fixed markup. You’re charged a predictable fee per transaction regardless of the customer’s card type. Since some cards are cheaper than others (debit cards vs premium credit cards for example) this can lead to unnecessary costs for certain payment mixes.

Interchange++ charges the interchange and scheme fee costs for the specific card used by the shopper. When interchange fees go down, your costs go down. You get to see exactly what you are charged for every transaction and there’s no danger of hidden costs or additional surcharges.

Keeping cross-border payments simple with Adyen

So there you have it. Acquiring from all sides. It’s helpful to understand the benefits of cross-border vs local acquiring and the different types of payout and billing models. But ideally, you have a payments partner you trust to take care of all this for you.

Our global acquiring solution is full-stack, meaning we take care of everything for your business, from authorization to settlement. With a single platform, you benefit from global reach with local licenses and local connections. And, since we control the whole flow with no third-party dependencies, the buck stops with us.

Click below for a more detailed insight into Adyen Acquiring and how it can optimize your cross-border payments.