Article

Credit card processing: Everything you need to know

How does credit card processing work? And how can you do it better?

If you accept payments, you almost certainly process credit cards. But how much do you know about the process once your customer hits ‘pay’? In the following milliseconds, that payment passes through several systems. If it’s successful, your customer goes about their day. If it’s not, well, you know how frustrating that is for everyone.

The more you know about your credit card processing, the more control you have over its outcome. This article will walk you through a card payment process and explain how, with the right information and technology, you can increase your card approval rates, your conversions, and ultimately your revenue. You’ll learn:

How credit card processing works

How to optimise your online credit card processing

How to optimise your in-store credit card processing

How credit card processing fees work

How we can help

How does credit card processing work?

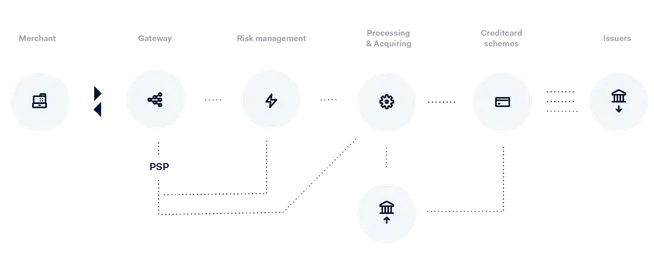

Here’s a breakdown of how credit card processing works step-by-step:

The shopper enters the merchant's store or website and goes to pay.

They enter their details via the payment gateway (or checkout) and hit 'pay'.

The risk management system checks the transaction to ensure it’s not fraudulent.

The acquirer routes the transaction via the card schemes (Visa, Mastercard, Amex, etc.) to the customer’s bank and requests authorisation.

The payment processor receives a response from the acquirer and either processes the payment or tells the merchant it was declined.

If the payment is authorised, the money is settled into the merchant's bank.

That’s a whole load of action, which should happen incredibly quickly. If it goes well, neither you nor your customer should notice it. But, as you can see, there are plenty of potential failure points along the way. This is especially the case if you have different providers taking care of each step. Systems don’t connect properly, or they time-out. The result: failed payments.

Here’s a sobering stat for you: 25% of declined card transactions lack valid reasons. That’s why we do things differently.

Our approach to credit card processing

Adyen was built back in 2006 by a team who’d worked in the world of finance and payments for years. They were only too familiar with the existing mess of legacy systems through which payments would trundle, getting stuck, blocked, or simply lost. So they decided to build a brand new system that took care of credit card processing end-to-end. Not just credit card processing, but local payment methods, online banking, ewallets, the works.

The Adyen payments platform handles the whole payment process from the moment your shopper hits ‘pay’ to the point the money lands in your bank. No third-parties, no patched-in systems; the buck stops with us. This full ownership of the process means we have the visibility and the tools to monitor each transaction and make adjustments in the background to ensure it has the best possible chance of success.

“The main change for us after partnering with Adyen is that we now treat payments as a conversion-driver.”

Bryony Longden

Senior Ecommerce Manager, Hunter

So what else drives a successful credit card payment? Let’s take a look at how you can optimise credit card processing online and in store.

Optimising online credit card processing

Getting your customer to the point of payment is an achievement in itself. A great checkout will make it easy for the customer to complete the payment, helping you close the sale. Here are some ways to ensure your online credit card processing runs as smoothly as possible:

Make your checkout easy to use

Speed your customer through the checkout process with these conversion optimisers:

Mobile-friendly, responsive design

Relevant choice of payment options, from cards, to ewallets and local payment methods if you’re selling overseas

No redirect: keep your customers on your site

Clearly displayed security logos

Block fraudsters, not customers

Risk management is both a science and an art. Set your defences too high and you’ll block legitimate customers; set them too low, and you’ll leave yourself vulnerable. The answer lies in data. The more data points your risk manager has, the more accurate its response. With information such as IP, email address, phone number, and postcode, a risk engine can run a check across its platform, identify patterns, and stop fraud before it happens. So, the more data you can capture at the checkout, the better.

Ensure uninterrupted subscriptions

If you run a subscription service or process recurring payments, you’ll want these to go through every time. Here’s how to achieve unstoppable subscriptions:

Keep your cards-on-file up-to-date with automatic ‘account updater’ services that ensure card details are correct even in the case of lost or expired cards

Automatically retry transactions that failed for technical reasons within milliseconds

Fine-tune your billing strategy to take pay-day into consideration

“When it came to the collection of our monthly subscription fees, our biggest challenge was the resource to remind customers when their subscription was due.”

Ruth Vero

Head of Customer Operations, GoHenry

Optimising in-store credit card processing

If you’re accepting credit cards in store, or at the point of sale (POS), you’ll want to ensure the process is quick and easy. Long queues are a big turn off for shoppers and, in a world of social distancing, unnecessary interaction should be kept to a minimum. Here’s how to optimise your credit card processing in store:

Contactless

Tap-to-pay is standard these days, and, since everyone wants to keep their distance, you can take contactless one step further and let customers pay via self-service kiosks.

Ewallets

Ewallets are easy to use and secure. Apple Pay and Google Pay™️ have the added benefit of helping to blur the lines between online and point of sale transactions so your customer can move seamlessly between the two. Amazon Pay lets customers pay using information already stored in their Amazon account. In all cases, they remove the need for customers to go digging around in their wallets.

Mobile point of sale (mPOS)

There’s a lot to be said for bringing the payment to the customer and not sending them off to join the back of a queue. Mobile point of sale (mPOS) terminals provide greater flexibility by letting you take payment from anywhere. Now, there’s a new generation of smartphone-style terminals that let you manage several POS functionalities from one device.

If you're weighing up POS options across multiple locations or verticals, our guide on how to choose the best POS system for enterprises breaks down what to prioritise, from terminal fleet management to vertical-specific hardware.

Credit card processing fees

As we mentioned at the beginning of this article, credit card payments goe through several steps, each of which carries a charge. Here’s a breakdown of your credit card fees:

Processing fee: Charged by your payment provider for processing the transaction

Card scheme fee: Charged by the card schemes for using their network

Interchange fee: Charged by the customer’s bank

Acquiring fee: Charged by the acquirer

These fees vary depending on the type of transaction, your location, and business model (to name but a few). It’s confusing, but it can have a significant impact on your bottom-line. Interchange fees are usually the biggest expense when it comes to credit card processing. They're also the biggest headache. The structure and fees vary for each market, as do types of cards (consumer debit, commercial debit, pre-paid, and so on). And they change all the time. Fortunately, there are ways to bring your interchange fees down:

Local acquiring

Just like mobile roaming fees, transactions are generally cheaper if processed locally. It’s better to use a local acquirer where possible because this is the only way to benefit from local regulations and incentivised fees.

Incentivised fees

Interchange fees vary from market to market. For example, In the US and Australia, Visa and Mastercard grant lower rates to specific businesses like charities, travel agents, streaming services, and utilities.

Adyen’s credit card processing fees

For every transaction that passes through our system, a small amount is deducted and distributed as follows:

Processing fee

Charged by

Adyen

Acquiring fee

Charged by

Adyen

Interchange fee

Charged by

Customer's bank

Scheme fee

Charged by

Visa/Mastercard/Amex etc.

Exact costs will depend on factors such as transaction volume and location etc.

Why choose us for your credit card processing?

When you’re setting up your credit card processing, you’ll need a payment gateway, an acquirer, a risk management tool, and a payment processor. If you’re selling in store as well, you’ll also need a POS terminal provider and in-store payments processor. If you’re operating in different regions, this set-up quickly duplicates.

With Adyen, you get all of this in one. One global payments processor for all your channels, regions, and payments processing. This not only streamlines your business but gives you a single view of your payments in one system. You can track your performance and get to know your customers better. You can also offer customers total flexibility since it won’t make any difference to you where, how, or when they choose to buy. It all goes to the same place.

“A single payments solution with one back-office that can be rolled out seamlessly across multiple markets, payment methods, and currencies is a real game-changer.”

Neil Sansom

Omnichannel Director, Moss Bros

Data-driven fraud defence and authorisation rate optimisation come as standard. You don’t need to be a payments whiz; these tools work automatically. We’ll dig into the data and suggest adjustments to your settings.

Whether you’re integrating via your ecommerce platform, using our drag-and-drop elements, or building your own payments experience with our API, we’ve got you covered. And there’s always someone on hand to offer guidance if needed. Every customer gets a ‘first 90 days’ set-up service to make sure you’re set up for success, and you’ll always have access to ongoing support.

"When we started working with Adyen, we were both young and ambitious companies. We had mutual goals to grow our businesses as fast as possible. So it has been a mutual partnership."

Andy Wiggan

Director of Payments, Spotify