Reports

Evolution of payments: The payment industry explained

Learn about key players and big changes in this brief history, covering 40 years of evolution in the payment industry.

From gold coins to digital wallets, the way people pay and how businesses receive payments have changed a lot. But the current payment industry is a particularly complex space. Hundreds of companies offer payment systems and financial services that carve up the payment process into smaller, more intricate parts.

The evolution of payments over the past four decades

In this article, we’ll explore key players in the payment industry and the biggest changes in payment systems that have occurred during the evolution of payment processing over the years.

Plus, scroll down for definitions of 12 common payment industry terms.

The payment industry before the internet

In 1979, Visa introduced the credit card terminal. By the 1980s, electronic payment systems were the big hair and shoulder pads of the retail community. Their popularity grew fast, giving rise to hardware manufacturers like Hypercom, Ingenico, and Verifone.

The terminal transformed the roles of payment networks and payment processors. From paper voucher logistics companies, they evolved to become electronic communication providers.

In the pre-internet era, this meant constructing a network of telecommunications relays and data management platforms to provide electronic payment acceptance services worldwide. The terminal ecosystem has developed continuously since then. But the mid-90s arrival of the internet brought an entirely different mindset.

Internet-based businesses demanded a new kind of payment terminal: A virtual one compatible with the needs of online business. And a host of online payment processing companies, like Authorize.net, CyberSource, and Bibit appeared.

In those days, there were many barriers to enter the payment processing business. So these companies chose not to compete with big processors. Instead, they focused on creating merchant-and consumer-facing technologies and became known as payment gateways (definition below).

Payment gateways were the web-based equivalent of payment terminals, adapting internet-based transactions so that they could be retrofitted and funneled into pre-existing payment processors.

The rise of ecommerce (and payment gateways)

In 1994, a startup called Amazon.com opened for business. The next year, eBay launched. As online commerce ballooned, so did the volume of transactions passed from payment gateways to the payment processors.

Keen for a larger share of the pie, payment processors decided to absorb the payments gateway function into their systems, acquiring the best-performing gateways. But integration of these gateways was complicated – they soon found that migrating customers (and their transaction volume) to their platforms is tricky. Plus, with thousands of businesses generating billions of transactions, things started to creak a bit.

Meanwhile, the gateways flourished. These companies continued to specialise in specific merchant segments. Consequently, no single gateway could serve the needs of a processor’s entire customer base and so they had to connect with multiple gateways.

These legacy processors tended to retrofit new technology on top of the old. By the 2000s, merchants were integrating directly with payment gateways and routing transactions to a number of different processors.

At the same time, innovation in the payment industry was speeding up with solutions like:

Local data storage and processing power

Data encryption

Tokenisation

Mobile payments

Omnichannel

A new era of choice in the payment industry

Today, anyone running a company must choose from a dizzying variety of payment service providers to accept online and in-store payments and defend against fraud.

Banks offer payment processing, but often with a pile of disparate technologies, some of which was developed in the 1980s.

Gateway-only businesses process payments. But, since they play such a small part in the payments value chain, their technology must still plug into the old infrastructure.

Plenty of companies offer standalone fraud solutions. But investing separately in payments and fraud reduction technology means a business owner needs more people to manage separate relationships and integrations.

Each of these options require separate integrations and contracts. All of them come with their own reporting formats. Add point of sale systems and payment terminals, plus several markets with different payment preferences into the mix, and things really heat up.

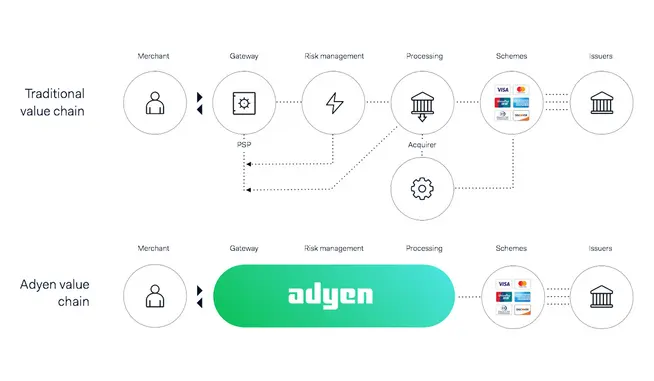

The core mission of Adyen is to make simplify payments for businesses. We take care of the whole payments value chain from checkout through to final settlement. This includes hundreds of payment methods, direct connections to card schemes, and protection against fraud. We also support in-store payments with payment terminals that accept everything from Apple Pay to Alipay.

With Adyen, you get all of this all in one platform – one global payments processor for all your sales channels, payment methods, and payment processing. Enjoy a single view of your payments set-up, while streamlining your business. Not only can you track your performance and understand your customers better, you can also offer customers total flexibility since they will be getting seamless, consistent payment experiences.

12 common payment industry terms

Payment industry terms can be confusing and acronyms abound. Authorisation rates? PCI? POS? PSD2? We’re here to help. Below are a dozen of the most common terms and phrases, along with their definitions.

Acquirer (or Acquiring bank):

An organisation which processes debit and credit card payments on behalf of businesses. Sometimes it’s a bank, but not always. For example, Adyen is an acquirer.

Authorisation

An authorisation happens when a card issuer (like a bank or credit card company) verifies a shopper’s request to purchase something. When approved, the issuer reserves the authorised amount in the cardholder’s account to prepare for the capture (actual funds transfer). An authorisation rate is the percentage of transactions that are authorised sucessfully.

Card networks (or card schemes)

The largest card networks are Visa, Mastercard, American Express, Discover, and UnionPay. They set the technical infrastructure and rules for payment processing and they charge for the service.

Chargeback

When a shopper does not agree with a charge on a card, they can ask for a refund. If the business refuses, the shopper can ask their bank to raise a chargeback. This is the starting point of a dispute process to define who is liable for the transaction. Reasons for a chargeback can include fraud, defective goods, or goods not delivered.

Fraud (fraudulent payment)

This means a transaction was either attempted or completed by a malicious agent. There are different types of fraud, including card-not-present fraud and triangulation fraud among others. Discover how you can better detect the risks and defend your business.

Interchange fee

The fee for a card-based transaction paid by the business to the shopper’s issuing bank (via the acquirer). The amount can depend on the card type, transaction value, and merchant category.

Issuer (or issuing bank)

The issuing bank (also known as the shopper’s bank) equips consumers with various types of cards, such as debit and credit cards.

Local payment methods (or alternative payment methods)

Any payment method that is not a major card network. Card payments are not the dominant method of payment in all markets. In some countries, payment by bank transfers, direct debit, digital wallets, or cash-based services are more popular. Discover popular payment methods from around the world, available with just a single integration with Adyen.

Point of sale (POS)

A point of sale solution is the combination of hardware and software that lets a shopper pay in person. It’s an important component of the payments ecosystem especially when it comes to offering convenient contactless payment options.

Payment gateway

Otherwise known as your checkout, the payment gateway helps businesses initiate ecommerce, in-app, and point of sale payments via a variety of payment methods. The gateway is not directly involved in the money flow; typically it is a web server which is connected to a business’ website or POS system.

Payment Service Provider (PSP)

A company that combines the functions of both a payment gateway and a payment processor and can connect to multiple acquiring and payment networks.

PCI compliance

PCI DSS (Payment Card Industry Data Security Standard) was created by the major card networks to increase the safety of cardholder data and reduce risk of fraud. All organisations involved with payment card processing must be PCI-compliant.