ADYEN INDEX: AUSTRALIAN INSURANCE REPORT 2026

The digital shift: Redefining insurance with smarter payments

Discover how payment solutions can be your strategic edge with insights on consumer trends and preferences in the insurance sector.

Overview

Embracing the digital shift

The insurance industry stands at a crossroads, caught between the pull of tradition and the push of digital transformation.

Customers today demand more than just coverage. They seek smooth online payment experiences with the flexibility to use their preferred payment methods.

Meanwhile, many insurers underestimate the role of payments and its impact on customer retention, fraud reduction, and staying competitive amongst emerging insurtech businesses.

We spoke to Australian industry leaders and insurance customers to map out the latest trends and consumer preferences. Here’s what we discovered:

1. Flexible, intuitive payments are a top factor in how customers select insurance providers.

Almost half of online customers want to purchase insurance through mobile-first channels.

Four in five of 25-34 year olds find insurance subscription models appealing.

Customers assess insurance payment experiences against sectors like retail and fintech.

2. The customer experience gap widens as insurtech businesses outpace many legacy players with effortless payments.

Insurtech businesses are leading the transformation in product offerings and payment solutions.

85% of industry leaders see payment processing as an integral part of the operations for insurance businesses.

That said, 28% of insurers recognise that the sector falls short in payment capabilities compared to other industries.

3. All insurers can use payments to achieve impactful gains.

Industry leaders say stronger payment capabilities offer insurers clearer payment statuses, consolidated payment platforms leading to reduced overhead costs, and automated reconciliations.

Innovative payment solutions can have a transformative impact by reducing fraud and improving the quality of customer experience.

Issues with payments create additional work and costs for insurers. One in four customers contacting service support faced payment issues when buying their policy in the last two years.

It’s not just about convenience.

Payment solutions can offer insurers a strategic advantage in the digital age — all without the need for massive system overhauls.

In a nutshell, the future of insurance is digital and the time to act is now.

“Many insurers have a payments blind spot. They don’t realise that modernising online payments could drive significant benefits for their business in terms of selling more policies, reducing operational costs, and driving down fraud.”

Chapter 1: The new standard

Flexible, intuitive payments are a top factor in how customers select insurance providers

Customer expectations are evolving as quickly as technology.

Demand for personalised, instant insurance products that offer better value, convenience, and intuitive experiences is inspiring a new wave of digital propositions.

Almost half of online insurance customers want to purchase policies through mobile-first channels.

Benchmarking the best, cross-industry

Customers today don’t just compare insurer payment experiences against one another. They now expect the best of the best, judging insurers by the standards set by top brands in sectors like retail, fintech, travel, and entertainment.

Customers rank retail as the top industry leading the way in online payments, far ahead of insurance.

Changing demographics

What’s more, Gen Z and Millennials are now a major segment of the insurance market and expect innovation and seamless digital customer experiences.

They’re particularly attracted to new concepts such as on-demand insurance, intuitive offerings from fintech apps, and embedded services.

Ease of payment has become a ‘top 4’ decision factor for this group when buying insurance, ranking above policy factors such as the claims process.

80% of 25-34 year olds find the idea of insurance subscription models appealing.

76% of 25-34 year olds prefer prepaid virtual cards to avoid being out-of-pocket during a claim.

“You can lose a whole segment of the population if you don't adopt and integrate the right technologies.” — Insurance industry leader

Streamlining pay-ins and pay-outs

For today's insurance customers, pay-ins (purchasing or renewing a policy) and pay-outs (settling a claim) can be a source of frustration.

Common pain points centre upon time delays, errors, and inaccuracies which can lead to customers being out-of-pocket.

For pay-ins specifically, friction can cause customers to drop out of the initial purchase journey or for policies to lapse.

“If a customer doesn't make their payment for two months, we have to cancel their policy — they don't have the cover and that's it. On the other hand, data could be used to give a good profile of the customer, tailor the product to meet their needs, and keep up affordable payments.” — Insurance industry leader

It can also cause serious operational challenges for insurers, such as forecasting and resource allocation. Within price comparison sites, even small amounts of pay-in friction can send customers back to consider alternatives.

“When a customer uses a price comparison website, it is integral to keep all that data, so the customer doesn't need to add it on your platform. As soon as you start asking extra questions, there's a dropout rate.” — Insurance industry leader

When it comes to pay-outs, customers can often find them frustrating due to long waits exacerbated by inflexible processes and rigid payment channels.

“Cheques nowadays are an inconvenience. The amount was so large I had to physically take it to a bank. It was a two-hour round trip.”— Insurance customer

Today’s customers expect both pay-in and pay-out experiences to mirror each other and are clear about their needs:

Ability to pay with method of choice

Customer needs when settling claims (pay-outs):

Fast payment resolution to avoid being left out-of-pocket

Saved payment information to avoid lengthy manual entry

Customer needs when settling claims (pay-outs):

Flexibility to receive pay-outs through payment channel of choice (e.g., digitally rather than paper cheques)

Mobile-friendly platforms allowing quick, secure, on-the-go payments (e.g. Apple Pay)

Customer needs when settling claims (pay-outs):

Proactive communication and transparency to see progress

Insurers are now recognising the importance of payments as a key differentiator in customer conversion, retention, and experience across the insurance lifecycle.

But we still have a way to go:

31% of insurers believe complex online checkouts have a significant negative impact on customer experience.

Key takeaway

There's a rising demand for payments innovation in this space.

For customers, the use of cheques and traditional processes are phasing out. Instead, they want flexible payment methods — like the ability to pay with digital wallets.

But there’s a disconnect between customer expectations and current insurer best practices. Case in point:

Although the insurance industry relies heavily on bank direct debits, customers want to use credit cards (55%), debit cards (53%), or digital wallets (42%) to pay online.

While integrating new payments technology is the first step, making use of payments data plays a critical role too.

With it, data can be leveraged to gain a deeper understanding of customers’ buying habits, risk levels, and product preferences.

This level of personalisation unlocks the ability to better meet (and exceed) their expectations.

Chapter 2: A competitive edge

The customer experience gap widens as insurtech businesses outpace many legacy players with effortless payments

Insurtech businesses are challenging traditional firms to move quickly in order to stay relevant.

“I see insurtechs changing the sector because they're not scared to do so…this is what the sector has got to go through. I think it’s for the better.” — Insurance industry leader

A more competitive environment As models such as embedded insurance continue to rise in popularity, insurers will need flexible payment structures to enable them.

And while many incumbents have invested in digital infrastructure, product and channel innovation is key to staying competitive.

“Apathy is one of the scariest challenges in insurance today. There is a tendency among traditional insurers to not take [innovation] seriously.” — Insurance industry leader

Many newer players use data at the core of what they do and have systems that talk to each other, allowing them to be agile and better meet customer preferences.

“If insurers aren’t providing customers with a good service, they’ll simply switch to another insurer.” — Insurance industry leader

Industry priorities highlight payment innovation opportunities

Both traditional and new firms see data-driven decision making as important, with other factors like product innovation and customer retention top of mind too.

Interestingly, the key areas that insurers want to prioritise can benefit from integrating innovative payment solutions.

That said, many insurers from traditional firms haven’t yet realised the full extent of the impact of payments:

“The word ‘payments’ is almost never discussed around the boardroom table. Insurance leaders are rightly focused on delivering better digital experiences, reducing the cost to serve, and managing risk and fraud. But payments can play a central role in helping them achieve all three of these corporate priorities.” — Adrian Davis, Commercial Leader, Financial Services and Insurance, Adyen

With the right focus and capability, payments can be elevated to support a range of key strategic priorities.

“The importance of holding on to your customer after acquisition has never been truer. But what can you do other than price? It's got to be about ease of transaction, ease of renewal, and simplification.” — Insurance industry leader

Key takeaway

Payments are more important than many traditional insurance firms realise.

While there is recognition that payments can simplify processes, looking at it from an operational standpoint is only one piece of the pie.

85% of professionals say payment processing is integral to operations.

In order to stay competitive, insurers need to reimagine how they integrate payment solutions.

“You differentiate yourself from other insurers by the speed and ease of your payment systems.” — Insurance industry leader

And it doesn’t require a huge lift.

It can be as simple as improving the customer experience with easier sign up processes or minimising fraud with payment tokenisation.

The time has come for insurers to consider the value and opportunity of payment innovation, or risk falling behind.

Chapter 3: The path forward

All insurers can use payments to achieve impactful gains

There’s significant variation in the core technology used by insurance firms.

Some retain legacy technology platforms while others have undertaken complete digitisation.

Technology overview

Legacy core system

On premise, monolithic architecture, old technology. Functionality limited by the platform.

Mix of digital and legacy

Digital and integration capabilities, but with some reliance on wider legacy capabilities.

Digital to the core

Cloud native, open architecture, thinner core, larger footprint for external ecosystem of modern capability.

Typical payments capability

Legacy core system

Payments are often viewed as a low-value function and have received limited investment. Capabilities are limited and fragmented.

Mix of digital and legacy

Some appreciation of digital payments but many systems remain fragmented and full value is not being realised.

Digital to the core

Good understanding of the value of modern payments. Focus is on leveraging payments as a strategic capability.

Suggested focus areas

Legacy core system

- Incremental steps including integration of wallets to improve customer experience.

- Consolidation of payment providers.

Mix of digital and legacy

- Understanding total cost to operate (TCO) and bringing this down through automation.

- Building consistency across channels to deliver efficiency.

Digital to the core

- Optimisation of journeys via modern payment providers.

- Fully developing the use of payments data.

A representation of the different stages of digital transformation for insurance firms and how payments can support

Implementing new digital payment technology can feel like a challenge for incumbent insurers with legacy infrastructure.

However, payment modernisation is key to solving customer and business pain points.

“Wholesale transformational change in legacy insurance is undoubtedly tough, but modernising your payments can be achieved quickly, with an immediate payback. We recently onboarded one of the world’s biggest insurers and within 48 hours we were live; processing pay-ins and pay-outs.”

The benefits of this investment are partially understood:

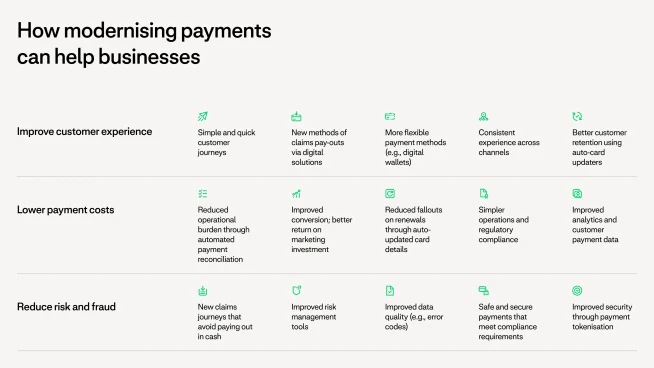

36% of insurance professionals see the benefits of stronger payment capabilities for improving error detection and resolution.

54% say stronger payments can help increase transparency and communication of payment statuses.

But the benefits reach much further:

For further innovation, insurers can also benefit from insights and capabilities honed in other industries:

Subscription economy: Leveraging insights on optimal billing cycles per region, and experimenting with “retries” for failed payments.

Retail businesses: Unified omnichannel payments, supported by machine-learning models to increase authorisation rates and reduce fraud.

Online marketplaces: Capabilities such as onboarding, tracking, and split payments to meet the array of customer needs.

Fintech companies: Pilot testing with small groups of customers to gather feedback and identify issues before wider feature rollouts.

Conclusion

There’s a digital gap in insurance and payments is the way forward.

While every business’ approach will be different, both legacy players and industry newcomers can benefit from a strong payments strategy.

With a range of innovative payment tools and solutions, insurers can:

Improve customer experiences.

Reduce the cost to serve.

Better prevent and respond to fraud.

Stay competitive in an evolving market.

“Payments must be intrinsically linked to the overall architecture of what you're doing. If you're going to be digital, then your payment platforms must be digital too. The experience needs to be seamless.” — Insurance industry leader

Let's talk

Adyen serves over 50 global brands across the insurance market. From top insurers to leading insurtechs to large brokers, we have an unrivalled view of what insurers need to make the most of digital payments.