Reports

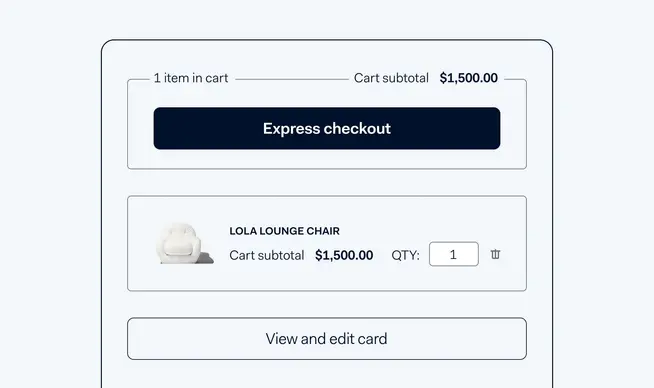

Express checkout: Three ways to pay in one click

Discover the differences between an express checkout, one-click payment, and an express payment method and what all three can bring to your business.

A fast and frictionless checkout process can dramatically increase your conversion rates. That’s why businesses are constantly looking for new ways to improve the checkout experience.

What is express checkout?

The latest fast-growing approach goes by various names like express checkout, express payment methods, one-click checkout, Click to Pay, instant payments, one-click payments, Checkout as a Service, and maybe a few more we don’t even know about. As a category, they can be referred to as "express flows".

The aim of express flows is simple: let customers check out and pay with the least amount of clicks.

They've transformed the online buying process. What once required customers to manually fill in many form fields can now be achieved in a few clicks. Express flows make this possible by storing payment details and sometimes shipping and billing information.

Is there a difference between express flows?

Despite being similar, there are several key differences between express flows. The key difference is where the customer details are stored:

When a customer saves payment details for later or creates an account, the merchant stores the data

For Click to Pay or express payment methods, the data is stored by the payment method

For one-click, express checkouts or Checkout as a Service, a third party checkout provider stores the data

Let’s explore these express flows further and weigh the pros and cons of the available features and implementation times.

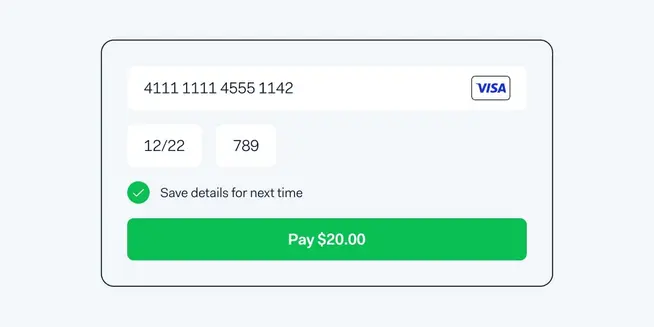

1) Storing customer details with the merchant

This type of express flow has been around the longest. Customers can use their payment and delivery information for future purchases when they check out by saving their details for later or creating an account. The next time they shop with the same merchant, the customer’s details are pre-filled after logging in.

As the customer only stores their details with one merchant, this type of express flow can indicate brand loyalty.

This express flow can store two kinds of data:

Name and address information. Usually stored in the merchant’s platform and should comply with privacy legislation.

Payment details. When stored, tokenization replaces sensitive data with non-sensitive data. A party that is PCI DSS compliant can save these details. That could be the merchant, but it’s more common to store these sensitive details with a Payment Service Provider (PSP).

This express flow type is relatively easy to implement as you or your PSP stores the information. It’s mostly relevant for returning customers. If the majority of your customers are first-time buyers, another express flow type might be more beneficial.

Relatively easy implementation

Cons

Not available for first-time customers (only for returning)

Account creation, tokenization, and a checkout familiar to the customer all result in a very fast flow

Cons

Customers can only reuse saved details with one merchant, which might not incentivize them to make an account

Can be easily combined with loyalty programs, connected to the customer’s account or email address

Cons

2) Storing customer details with a payment method

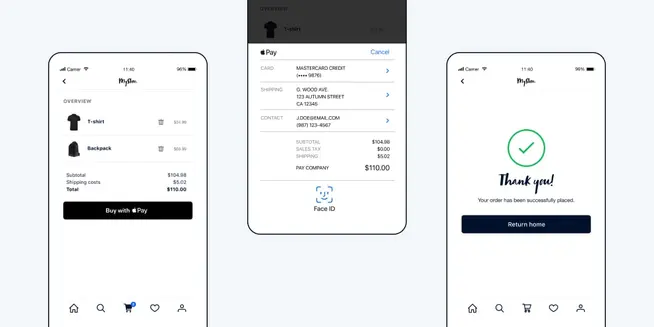

Express payment methods are a newer addition and catching on fast. The customer’s personal information and payment details are stored and provided by the payment method.

The customer sees a button with a payment method's logo, usually on the checkout page. To make a payment, the customer clicks the logo and (if they’re not already) logs in to their account with the payment method. They also might need to confirm the payment with facial recognition, a password, or another authentication option (each express payment method has its own authentication flow).

Many payment methods offer an express flow, including Apple Pay, Google Pay™ and PayPal. Others are being released soon, like Click to Pay and an express flow offered by iDEAL.

To implement, you need to add a payment method button to your preferred pages. We’d advise adding only one or two express payment methods to the checkout so you don’t risk overwhelming the customer.

Because the spots are limited, competition is fierce. Each payment method strives to make its offering as attractive as possible for customers and merchants. They work on increasing conversion rates, making implementation easier, improving customer convenience, and providing options like Buy now, pay later.

Available for first-time and returning customers

Cons

Can be challenging for older ecommerce platforms to implement and create a seamless experience

Customers can use this express flow across multiple sites and merchants

Cons

Usually can’t offer more than two express payment methods at checkout

Creates trust early in the checkout, as the customer is familiar with their preferred payment method

Cons

Depending on your vertical and the page design, offering an express payment button on the product page might lead to a lower ATV

If implemented through your PSP, you can access the same reporting and authentication features you have with your PSP

Cons

Each express payment method might provide addresses in different formats, so you need to map this data correctly

3) Storing customer details with a third party checkout offering

Some companies work only on offering a checkout that focuses on speed. “One-click checkouts”, like Bolt, let the customer pay in (basically) one click. “Express checkouts” let customers pay in one or more clicks.

Like the express payment methods above, the customer can pay almost instantly by clicking the express checkout button. The customer needs to have an account with the third party checkout and log in, though some services let first-time customers sign up in the checkout flow.

If customers have had a good experience with a specific express checkout provider, their logo in your checkout could instill trust. Some express checkouts go a step further and let customers buy your products directly through their site.

On the implementation side, you need to add an express checkout button to the product page or replace the checkout with this third party checkout entirely. If the merchant already has a PSP, this same PSP handles express flow payments. But if the merchant doesn’t have their own PSP, payments can sometimes be managed by the third party checkout’s PSP.

The payment features offered by a third party checkout might be more restricted than integrating with a regular PSP. We recommend double-checking whether the third party checkout meets your demands on robust reporting, authentication, account updater functionalities, or network token services. If you have any specific fraud and risk requirements, reconciliation and bookkeeping might be challenging.

Available for first-time and returning customers

Cons

Implemented on top of your existing ecommerce platform, which might result in technical and maintenance challenges

If the adoption rate is high with your target customers, it could boost conversion

Cons

Probably the most expensive of the three. Express checkouts often charge an extra fee.

Customers can use this express flow across multiple sites and merchants

Cons

Advanced, innovative payment features and risk checks might be limited.

Cons

If the third party checkout’s PSP handles the payment, your reconciliation and backend integration also need to support the PSP integration

Is an express checkout right for your business?

If the ease and speed of checking out is a friction point for your customers, it might be worth implementing one of the express flows above. We’d also advise considering:

Your first-time vs. returning customers

Option 1 (storing payment details with the merchant) is only relevant for returning customers. Options 2 and 3 (storing details with a payment method or third party checkout) are most useful for first-time customers.

Your business’s industry

An express flow can be particularly valuable to companies that deliver physical and digital goods (e.g. ride-hailing apps or in-game purchases).

Average Transaction Value (ATV)

If your ATV is over $500, the customer might want to consider their order carefully rather than check out fast, so an express flow may not be particularly valuable.

Ready to get started with an express flow?

Making the payment process seamless could give you the edge over the competition and may eventually become expected across all industries. The growing number of express flow options coming to market, either as a payment method or a third party offering, also reflects this trend.

If you decide to move forward with implementing an express flow, there are a couple of points to consider on the practical side, like:

Button placement

Where you decide to add an express payment method or checkout button can have some consequences. Placing an express flow button on a product page could increase purchases but negatively impact ATV. Adding several buttons to your product pages could also detract from the brand experience.

Every business values different strategies and metrics, so it’s crucial for you to monitor the effects of express flow and adjust where necessary.

Technical challenges

Besides how the checkout looks and performs, there are some complications to watch out for behind the scenes, like:

Address form field mapping. As the customer no longer fills in their details, you’ll need to request this information from somewhere else. This might require your tech team to map certain fields.

Pick up points. Sending a product anywhere other than the customer’s pre-saved address can be difficult. If you want to offer this service, you’ll need to consider an additional checkout step where the customer can edit the shipping details.

Strong customer authentication (SCA). Under Payment Services Directive 2 (PSD2), an extra step like 3D Secure to authenticate the customer could mean checking out in one click isn’t really possible.

Backend integration. Beyond integrating with the frontend, you might need a new backend or reconciliation integration.

Risk challenges. If fraud is a serious problem, assess your risk and fraud needs.

With Adyen, you can offer the express payment method that best suits your business. You can provide a straightforward checkout process while benefiting from high authorization rates and lower transaction fees through Adyen Acquiring and advanced risk management products.

Reach out to our sales team for more information or visit our documentation for technical insights on how to implement express payment methods.