Reports

Payments 101: Getting the most out of your payments set-up

Leverage payments as your secret weapon to success. Your payments set-up is crucial to remaining agile, streamlining your operations, and boosting your customer experience. Explore how payments work and how Adyen can help you realise your business ambitions faster.

There's a lot to keep in mind when running a business geared for success – distribution and logistics, marketing communications, and customer service. With new avenues, opportunities, and markets to pursue, the complexities can only increase. Payments might be easy to overlook as a commodity, but you're missing a huge opportunity to streamline your operations and drive further growth.

When done right, payments can unlock more revenue and keep you ahead of the curve in your industry. Learn more about the entire payment process and how to get the most value from each stage.

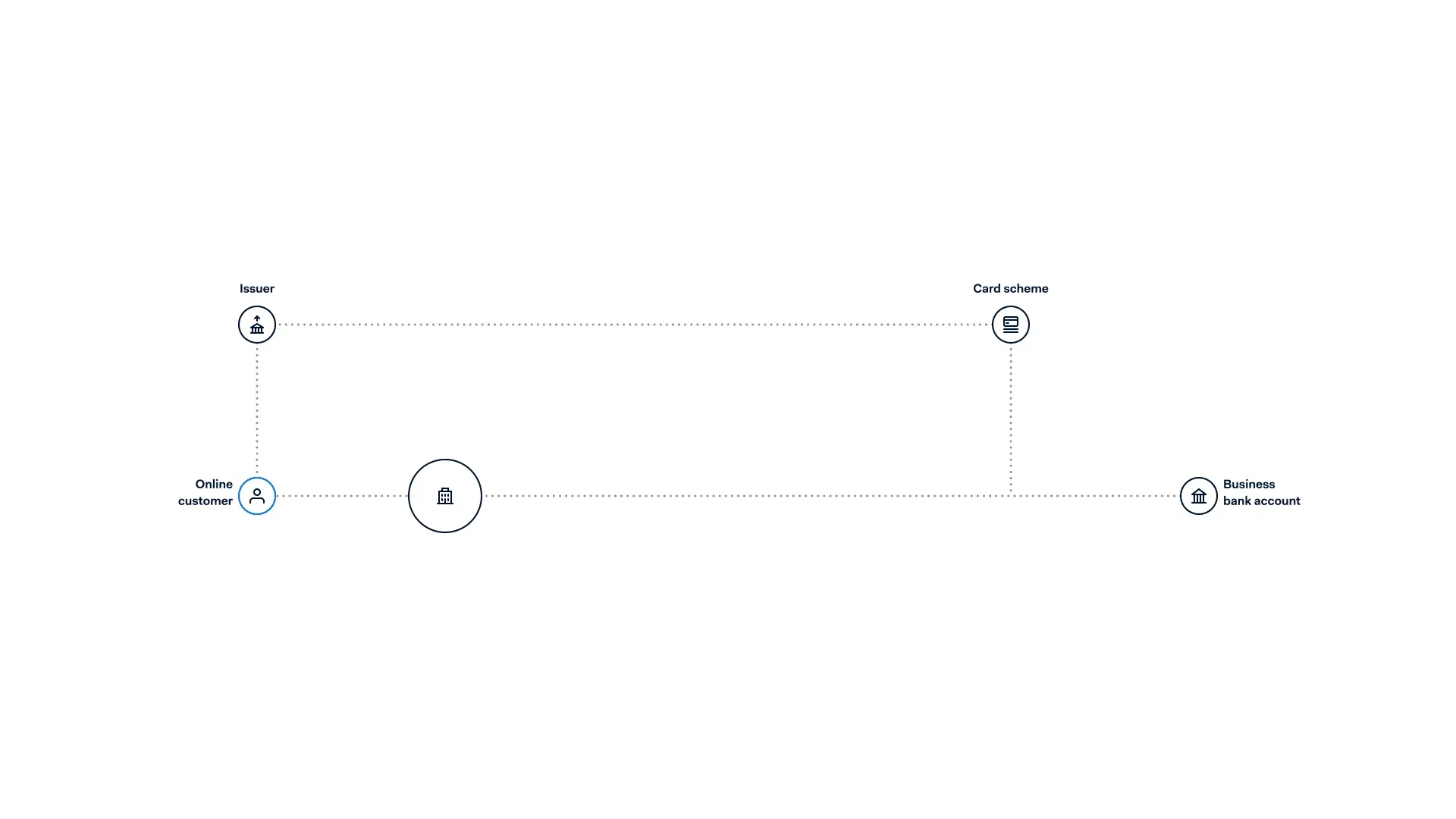

Key elements in payments

The world of payments is ever-evolving, with global events and new technology changing how people pay. In today's world, digital and physical worlds collide when it comes to how consumers browse, order, and purchase items or services. The days of cash-only payments are over, and methods such as digital wallets and QR codes are on the rise.

Let's take a closer look at the breakdown of the payment process.

Acquiring

Connects to the customer's issuing bank and requests authorisation.

Gateway

Processing

Receives a response from the acquirer and processes or declines the payment.

Risk assessment

Settlement

The transfer of money to your business.

Each step along the way provides opportunities for optimisation. Read on to find out more.

Boost your sales conversion rates

As the narrowest part of your sales funnel, it's vital that you get your checkout right if you want to turn each transaction into a loyal customer. As inflation and cost of living increase, Australian consumers are increasingly more discerning, with 62% of them abandoning their physical and digital cart if they can't pay how they want to.

Customers are already past the tipping point of yes or no at checkout. You're in the perfect position to give them exactly what they want, and it boils down to a flexible and seamless payment flow to turbocharge your conversion rates. There are many ways to boost your checkout conversions, but a long line at the till or a faltering online checkout are absolute no-nos.

Online checkout optimisation

Here's how to create an online checkout that will keep your customers coming back again and again.

Optimise the checkout page

It's crucial to ensure that every payment experience that potential customers go through is quick, easy, and secure. The entire payment flow and process should be hosted on the website to streamline and speed up the checkout process while maintaining total control over the branding and layout of the page. This in turn leads to a greater sense of trust between you and your customers.

Think mobile first, second, and always

Forecasts predict that smartphone users will rise to over 7 billion by 2024, while mobile transactions will reach a whopping $9.4 million by 2025. It's safe to assume customers often browse and pay for goods and services via their phones or tablets.

It's no longer a matter of just supporting mobile – you have to do it really well. Test your checkout page on multiple devices and operational systems and, on mobile apps, opt for in-app payments for a smoother payment flow instead of redirecting shoppers.

"The goal in the future is that there is less and less friction at the time of purchase and that transparency and security are prioritised. Z&V's digital teams were strengthened with this in mind, in order to remain at the forefront of the digitalisation of retailers."

Jonathan Attali

CDO, Zadig&Voltaire

In-person payments optimisation

Although consumers enjoy the convenience of online shopping, 63% of Australian customers still prefer shopping in stores because they are able to better gauge the fit and quality of the products. Just like online checkouts, in-person payments need to run smoothly to maintain your brand reputation and meet the increasing demands of your customers.

Bring payments to the customers

Few things are more off-putting than queueing to pay at a busy checkout. But things are changing – heavy hardware and separate cash registers are no longer necessary to create the best in-person experience.

A great way to enhance your in-person payments is mobile point of sale (mPOS) terminals. Process transactions anywhere in your store with a wireless device easily carried to wherever your customer is.

Apple's Tap to Pay on iPhone is an option that enables you to accept all types of in-person, contactless payments, leveraging iPhone's built-in security features to keep data private. All you need is an iPhone – no extra terminals or hardware are required.

Embrace unified commerce

Connecting your in-person and online experiences creates seamless, channel-agnostic journeys that go beyond just payments. Your customers can transact, without friction, across different sales channels, devices and markets. Plus, instead of managing each interaction with separate systems, it's all consolidated into one.

And this is what consumers are looking for – 63% of Australian consumers say they would be more loyal to a retailer if they were able to purchase an item that was out-of-stock in store and have it shipped directly to their home.

"We used to work with many different POS systems, and the problem that we found was that if we wanted to make any changes to the POS, or if we wanted to get data rapidly, then we couldn't do it. Now, we can go to the customer rather than the customer having to queue and come to the till point. This has been especially good at Christmas, where we can queue bust and help our less-abled customers, who sometimes might feel intimidated coming to the till point."

Mike West

Digital Director

Let customers pay how they want

Being able to accept relevant payment methods is pivotal if you want your business to connect with customers around the world. Just like people have different food, fashion, and music tastes, their payment preferences differ too. In Australia, some consumers might use Afterpay, while others prefer paying via their credit or debit card.

The reign of digital wallets

Shopping via a smartphone means people have easy access to digital wallets. By linking cards, user accounts, or pre-loaded funds, customers no longer need to pull out a physical card to pay. Convenient.

The wallet stores all the information necessary to make a purchase while meeting the requirements of Payments Card Industry (PCI) compliance and Payments Services Directive 2 (PSD2, to be updated with PSD3 in the near future). A central part of PSD2 and 3 is strong customer authentication (SCA), a more robust means of authentication that requires two forms of authentication. These wallets are automatically SCA compliant, as the most updated standards are already seamlessly built in. And, thanks to tokenisation, it's safer, too.

One size doesn't fit all

With new payment methods emerging all the time, it's critical to be ready to anticipate and adapt to your customers' changing preferences. It's not about offering every single payment in every market you operate in but offering the right ones in the right locations. Consider the experience it creates for the customer, too – keep in mind demographics and preferred sales channels.

Pick a payments partner that can help you to offer the best payment methods per market and show the relevant payment methods and currencies for that customer, based on their IP address.

Strike the right balance between risk and revenue

According to the Adyen Retail Report 2023, close to half of Australian businesses surveyed face considerable costs from fraud and chargebacks. Fraud is also fast becoming a cause of concern for consumers – 61% of Australian consumers believe online shopping is becoming less attractive due to the risk, and 75% want businesses to communicate their online fraud protection measures better.

Having the right systems in place and ensuring your chosen payments provider prioritises risk is critical to staying secure.

Fine-tune your fraud protection

The needs of every business are different, and risk management needs to be tailored to meet your unique challenges. The key is to strike a sustainable balance between blocking fraudsters and genuine customers through detecting, preventing, and responding to fraud.

Detect: Recognise genuine customers and spot fraudsters across all your sales channels. Work with a payments provider using multiple machine learning models and theories to detect fraud. This way, you can cover all possibilities and avoid unintentional biases regarding locale, payment method, or transaction value.

Prevent: Maintain complete control and reduce operational workload by combining risk rules with machine learning. Using labelled data, payment authorisation details, and other data points to make decisions, the machine is "rewarded" based on its success.

Respond: Increase authorisation rates and reduce chargebacks by optimising your risk management set-up.

Keep chargebacks at bay

A chargeback is when a payment is reversed after a customer disputes a charge on their account statement. They were initially introduced to offer consumers an easy way to dispute suspicious transactions and to protect them from fraud. But with a longer process and costly fees, chargebacks can put your revenue at risk.

Preventing chargebacks is more important than defending them. Find out more here.

"With RevenueProtect, we've reduced our fraud from 3.5% to 0%. We've been able to deploy 3DS2 across our websites, and we've seen benefits of close to $1.4 million annually."

Noel David

General Manager of Finance, True Alliance

Grow your revenue

With your risk management in shape and ready to protect your revenue, you can think about ways to optimise and grow it. With the right combination of tools from your payments provider, you can ensure that funds are recovered.

Intelligent decisions get results

Want your payments to be processed and approved without a hitch and save those that fail or are declined? Bring in machine learning to support.

Authentication

Combine data and machine learning technology across compliance, transaction, risk, and issuers to select the best authentication method for each transaction. As a result, you're boosting authorisation rates while keeping your UX smooth.

Automatic retries and rescue

Payments can often be declined due to an outage or downtime in the patchwork of legacy systems that make up the traditional payment flow. With the right payments partner, certain transactions can be automatically retried within milliseconds of the initial decline. Additionally, software can be used to spot which transactions stand a chance of succeeding if tried again, so you can rescue those that failed.

Keep cards on file up to date

A card-on-file transaction is when a cardholder authorises a business to store their payment details. In addition to this, that same business is permitted to bill the cardholder's stored account.

But every month, 6% of payment cards are lost, stolen, closed, or have their expiry dates changed. When storing the cards on behalf of your customers, you have to ensure their details are up to date – even if the card is lost, stolen, or expired. For this purpose, the card schemes provide Account Updater services that let businesses and acquirers replace invalid card numbers with new ones.

"Compared to third-party integrations, we've seen our authorisation rate increase from 87% to 94.5% with Adyen. Improved authorisation rates means we increase the revenue received by our customers."

Will Nicholson

Head of Global Payments, ROLLER

Own your insights

There's a lot to be discovered and implemented from the data collated through payments. Not only can it inform big business decisions, but it can also boost customer loyalty through targeted experiences. However, in 2023, only 25% of Australian businesses use data-rich payments insights to make informed business decisions or drive marketing efforts.

The regulations

Before proceeding, you must ensure that you follow privacy and security standards applicable to your markets. For example:

Payment Card Industry Data Security Standard (PCI): This is crucial for businesses that accept credit card payments. Businesses must adhere to 12 security standards when handling credit card data, including accepting, transmitting, processing, and storing it.

Compliance with applicable privacy laws.

For businesses that accept payments in Europe, it’s important to follow these regulations too:

Payment Services Directive 3 (PSD3): This regulation pertains to payment authentication. However, it hasn't been implemented yet, which means that and still apply.

General Data Protection Regulation (GDPR): This regulation ensures that personal data is only used for purposes for which the customer has consented.

Dive into your insights

The payment has gone through; the money is taken from your customer's account and credited to yours. Now what? You have data that can be aggregated to provide valuable business insights.

Payments data can teach you about your customers and how to cater to them. You can benefit even more if all these insights from devices, sales channels, and markets feed into the same platform, giving you a global snapshot of your customers, all in one place. Paint a detailed picture of your customer's needs, wants, and preferences; target specific customer segments and develop existing relationships.

The power of unified commerce

Because everything is connected on the backend, unified commerce can give you exciting insights from your payment data. The data enables you to meet the rising expectations of your customers. 43% of consumers in Australia prefer businesses who remember their preferences and previous shopping behaviours to create a more tailored experience. Additionally, 27% are willing to give their data to a business if there's something in it for them, such as a discount or special offer. Leverage payments data from unified commerce to power your personalisation strategies.